The Big Picture

The disconnect between the physical world and the stock market was particularly evident this week as Wall Street rallied during the Capitol Hill insurrection. Stimulus and money printing continues to inflate the market and boost valuations. From that point of view, the outcome of the Georgia senate race in favour of the Democrats is believed to further increase borrowing and allow the ongoing reflation trade to continue. It is however considered unlikely that the razor thin majority that the Democrats will have in Congress will allow Biden’s administration to pass radical reforms, especially on the corporate tax side.

This week was the time of the Moderna vaccine approval in the UK and in Europe. The increase of doses that the various vaccines offer is helping the market retain a positive outlook for 2021 and beyond. The growing number of cases and deaths in the US as well as in the UK does not seem to cause significant concerns for investors who experienced an “everything rally” first week of trading in 2021. Studies and expert opinions about the efficacy of the vaccines on the new strains of Covid-19 keep coming in but do not steal the scene in the news cycles.

Market Performance

All indices were up this week: in the US the Nasdaq led with a 2.4% gain, followed by the Dow (+1.8%) and the S&P500 (+1.6%). The Stoxx rallied (+3.0%) and so did the Italian index (+2.5%) despite the possibility of a change of government. The Danish OMX20 finished 1.4% higher. The US Dollar lost ground relative to the Euro reversing the trend from the previous two weeks. Crude oil joined the markets in the rally while $Gold finished lower. $BTC-USD gained more than 30% in a single week and whizzed past the 423.6% fib.

Earnings

A handful of earnings were released this week. Notable ones include $BBBY and $CAG who missed expectations, and $STZ and $MU who beat on both the top and the bottom line.

In other corporate news, $FCA.MI and $UG.PA announced that they will begin trading under the ticker of the newly formed merger company Stellantis next week.

The earning season starts next week with the first batch of bank stocks.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend. Most Italian stocks traditionally pay dividend in late May, while US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio was up 1.7% whereas the weighted average of the relevant market indices finished 2.2% higher.

The financial stocks keep pushing higher: $SYF gained 5.4% and $DANSKE.CO jumped 8.2%; $BK added 5.6% and is now up 20% overall. Our Chinese stocks had a very good week with $TCEHY and $JD gaining 7% and 4.1%, respectively. There is an ongoing political battle between the US and China over Chinese stocks trading in the US which, while it has not affected our positions so far, needs to be watched closely.

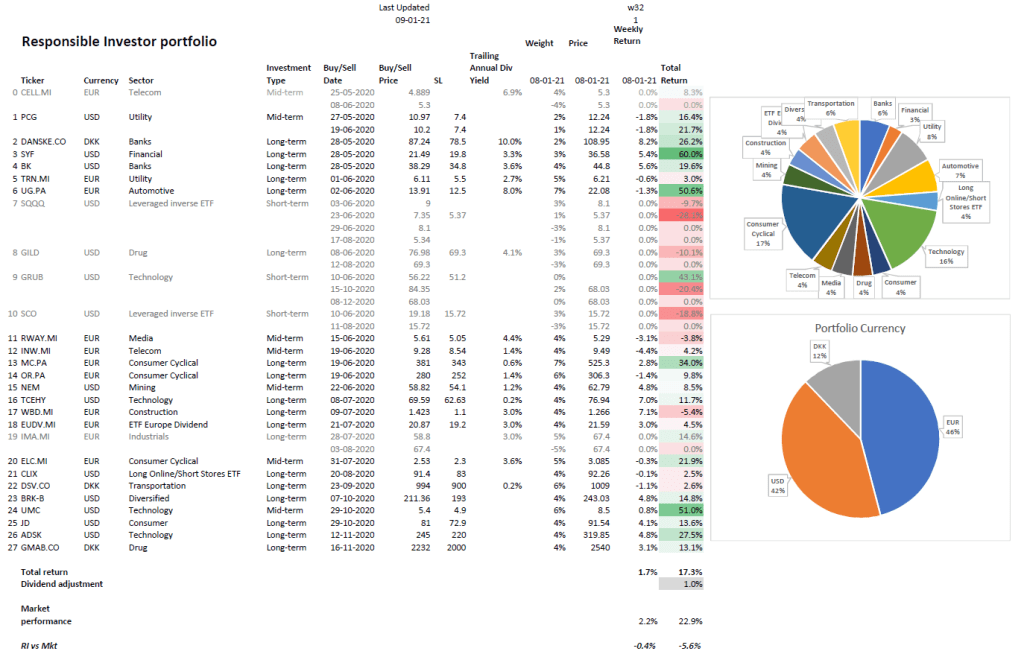

Our Responsible Investor portfolio is now up 17.3% (18.3% including dividends) in 8 months. We are about 58% in stocks & ETFs and 42% in cash. On my watchlist this week I have $DVA, $CMG, $MA, $CRWD, $AVGO, $LMND, $TRYG.CO and $ADBE.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.