Happy New Year everyone !

The Big Picture

The stimulus bills had just been passed last Sunday evening and discussions about increasing the checks for the American people from the agreed 600$ to 2000$ had already started. It really seems like the hiatus between election day and the start of Joe Biden’s presidency can only be filled with headlines about relief bills. Some attention is being drawn by the Georgia senate race which polls still indicate to be very close: the Senate currently stands at 50 Republicans and 48 Democrats; if Democrats win both runoffs, the party will have control of the chamber because Vice President-elect Kamala Harris would break any ties. But if Republicans win one of the two races, they will maintain control. The market is politically agnostic and only favours the latter outcome because it is seen as one which would not lead to a corporate tax hike. The S&P500 earnings prediction for 2020 is 140$ whereas the consensus for 2021 is 170$: Biden’s economic policy may affect this figure, however.

The UK approved the Astrazeneca-Oxford vaccine this week while the EU asked for more evidence of its efficacy and will need more time to give its verdict. It is a relief to start seeing the number of vaccine shots given to citizens next to the Covid numbers we are used to reading every day. The speed with which vaccinations will occur is likely to determine the speed of recovery for the economy in 2021. While the new strains of the virus cause some concern, this week´s market gains indicate moderate optimism: the test will come next week when institutional investors and money managers return from the Christmas break.

With Brexit now a reality, the EU managed to bring another trade deal home, this time with China. This agreement is considered particularly important given the size and growth rate of the counterpart and it strategically comes before Joe Biden is sworn in, in an attempt to anticipate his moves.

Market Performance

It was another short week for the stock markets as most European indices were only open the first two weekdays, the French and the UK indices adding Wednesday and US markets alone trading also on the 31st. All indices were up this week: in the US the S&P500 led with a 1.4% gain, followed by the Dow (+1.3%) and the Nasdaq (+0.6%). The Stoxx advanced 0.5% while the Italian index gained 0.5%. The Danish OMX20 finished 1.4% higher. The US Dollar appreciated relative to the Euro for the second week in a row and both crude oil and gold finished higher.

Earnings

No notable earnings were released this week. The next quarter’s earning season will start in mid January 2021.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend.

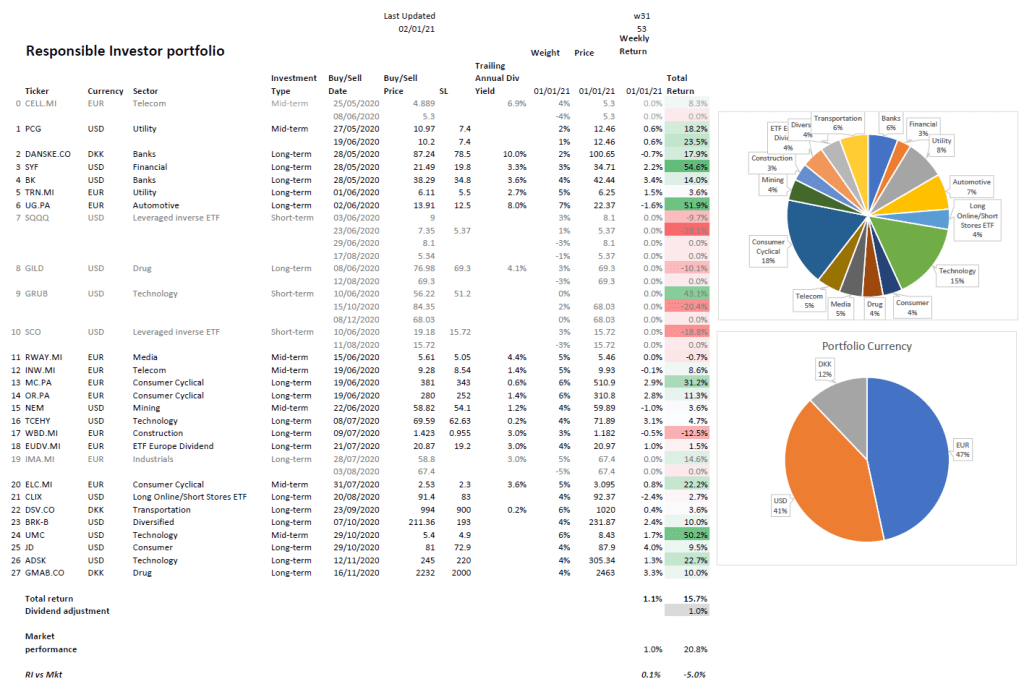

Portfolio Performance

Our portfolio was up 1.1% whereas the weighted average of the relevant market indices finished 1.0% higher, which means we had a marginal market beat this week.

The financial stocks had another great week: $SYF gained 2.2% and became our best performer in 2020 with a total appreciation of 54.6% (excl. dividends); $BK added 3.4% and is now up 14% overall. $TCEHY recovered some of the lost ground of the previous week by gaining 3.1%: it is worth noting that this company is ranked no. 7th by market cap, globally. We have had very good weekly gains on $MC.PA and $OR.PA which added 2.9 and 2.8%, respectively.

Our Responsible Investor portfolio is now up 15.7% (16.7% including dividends) in 31 weeks. We are about 57% in stocks & ETFs and 43% in cash. On my watchlist this week I have $DVA, $CMG, $MA, $CRWD, $AVGO and $ADBE.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.