The Big Picture

Our weekly blog returns after a week of gains for most stock markets with the notable exception of the Nasdaq which finished 1.5% lower and has now lost ground for the third consecutive week: if you are still holding on to the stocks which made great gains in 2020, chances are that you are in the red so far in 2021. There appear to be greater opportunities for capital appreciation in value stocks which also feature good momentum.

The jobs report unexpectedly disappointed and this fuelled a rally on Friday as retail investors pumped more money in the stock market on the assumption that heavy borrowing and low interest rates will continue indefinitely. Despite some of the indices hitting all time highs the risk for a correction is still there which is why it is important not to be fully invested at this time. Scroll below to see what percentage of our portfolio is in cash.

88% of the S&P500 stocks have reported their Q1 earnings so far: the numbers are impressive such that there are several analysts discussing the possibility of this past quarter coinciding with the peak in earnings which would suggest an impending bearish cycle.

Market Performance

Most of the stock market indices recovered this week following last week’s decline: in the US the Dow was the best performer with a 2.7% gain, followed by the S&P500 which finished 1.2% higher whereas the Nasdaq which finished markedly lower (-1.5%). In Europe, the Stoxx gained 1.8% while the Italian stock market was even stronger and finished 2.0% higher. The Danish OMX20 is on a bullish 9-week streak and was 1.0% higher this week. The US Dollar lost 1.1% on the Euro. Crude $oil gained 2.8% and $Gold showed great strength by appreciating 3.6%. $BTC-USD swung within a 10% range and finished 2.1% higher.

Earnings

Eight of our stocks reported Q1 earnings the week before last:

- DSV beat on earnings and revenue

- DANSKE beat on net profit

- ORSTED missed on revenue

- SYF beat on earnings and revenue

- UFC beat on earnings and missed on revenue

- NEM missed on both the top and the bottom line but the

- PCG missed on earnings but beat on revenue and reaffirmed guidance

- BRK-B beat on earnings.

$GMAB announced their Q1 earnings on Wednesday with solid gains compared to the same quarter in 2020. The company reported a five-fold increase in operating results and maintained the guidance for 2021 set out earlier in the year. $ELC.MI reported their earnings on the same day and beat consensus as well as raised their guidance: we have a 4.4€ target price on this stock which is already up 41.4% since we bought it.

Next week $JD and $INW.MI will report their Q1 earnings.

Dividends

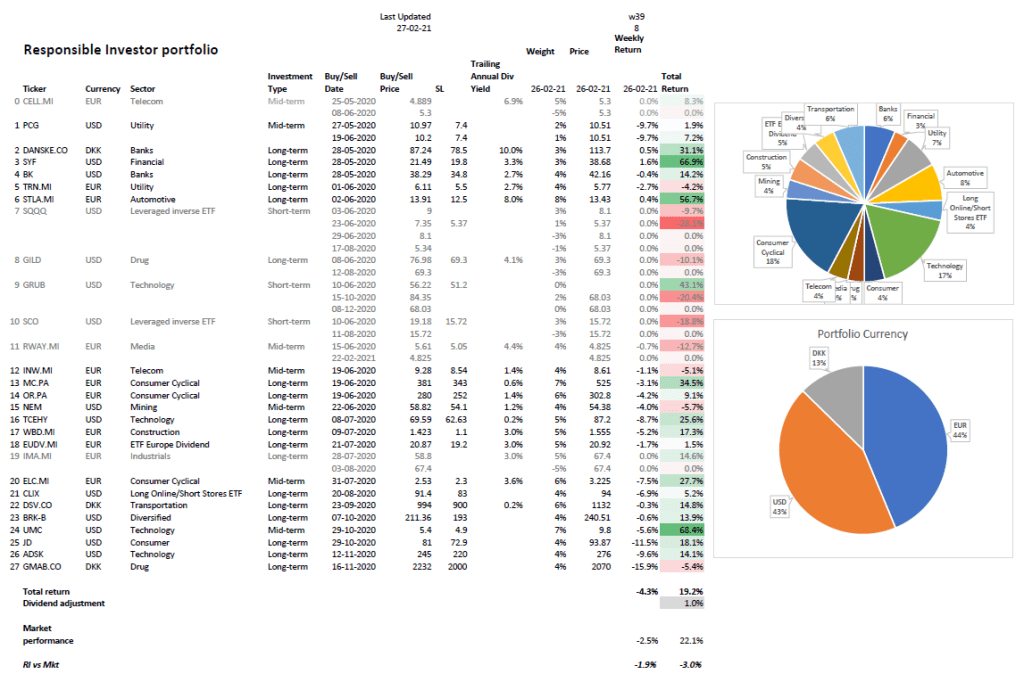

$OR.PA and $STLA.MI paid their dividend the week before last: our total dividend yield so far is 1.3%. Next week $WBD.MI goes ex-dividend. Our Danish stocks paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 1.8% this week whereas the weighted average of the relevant market indices finished 1.5% higher, which corresponds to a 0.3% market beat.

This week’s portfolio winners were $STLA.MI which was up 8.1% and mining company $NEM which gained 7.9% (+16.6% since initiation) helped by gold strength.

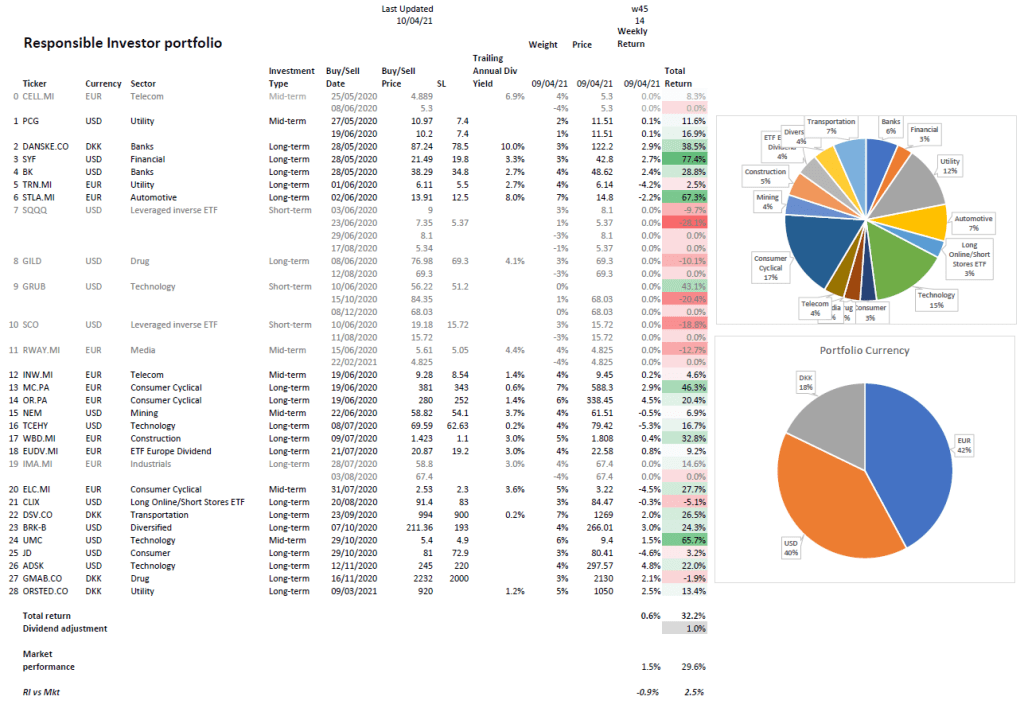

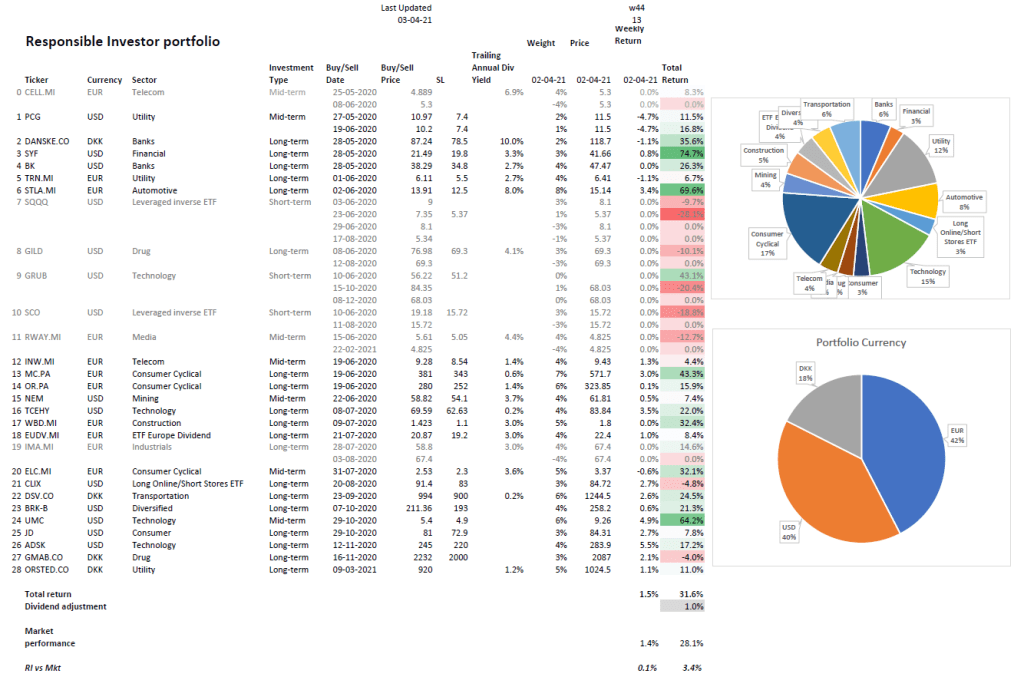

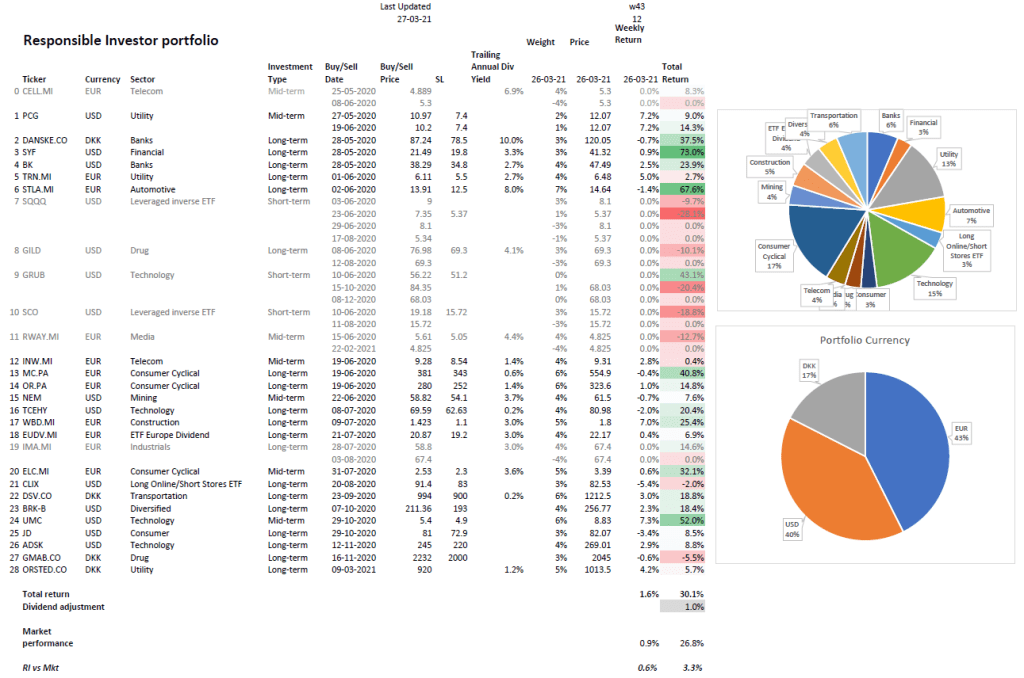

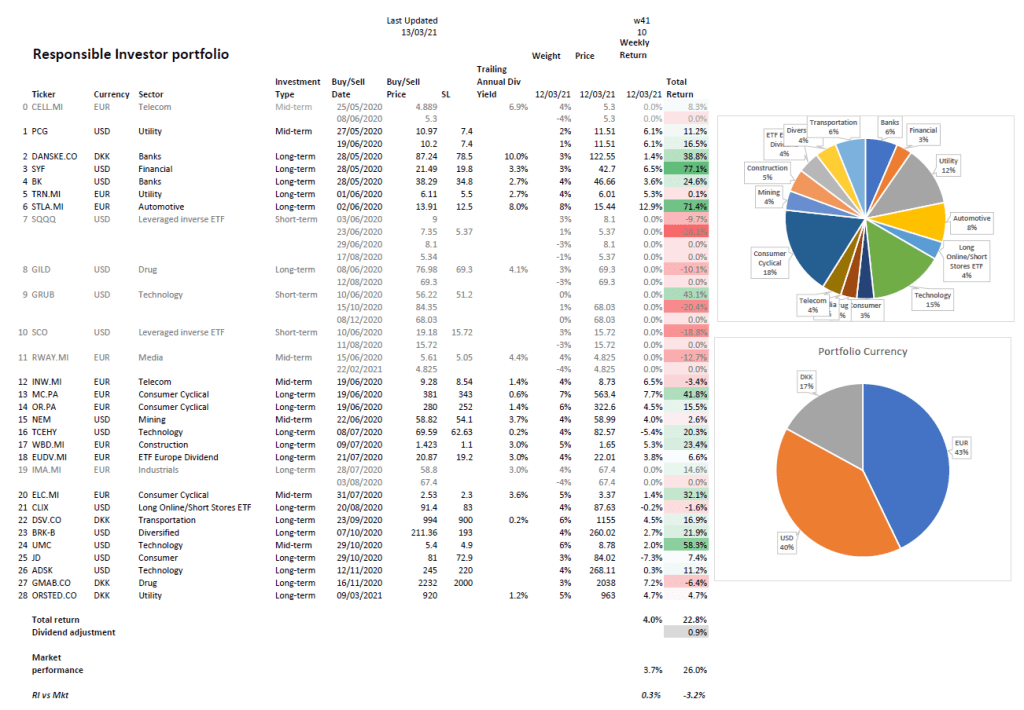

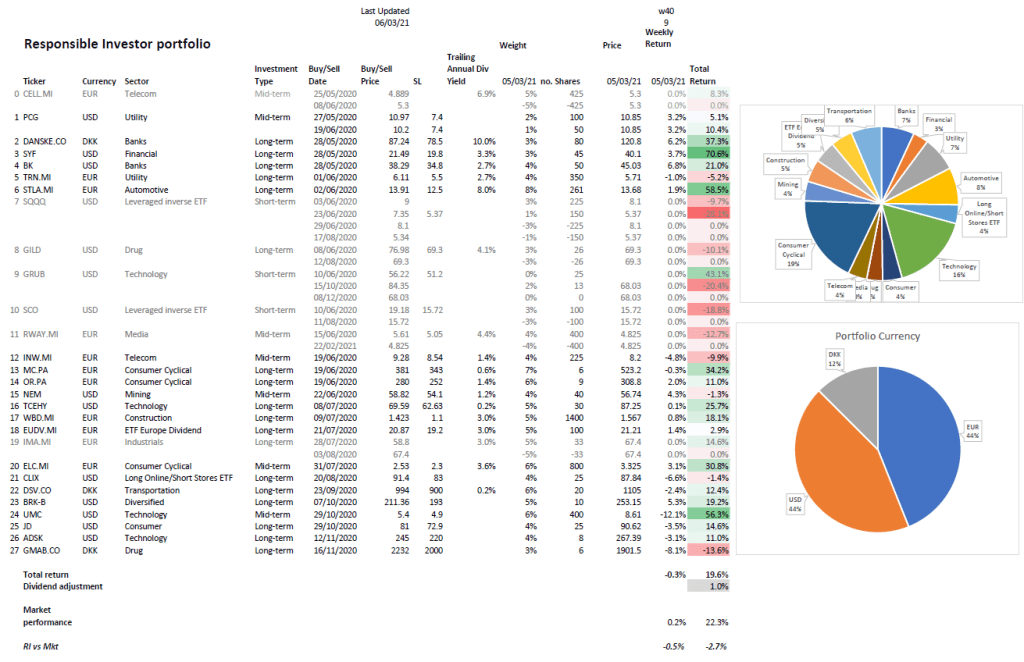

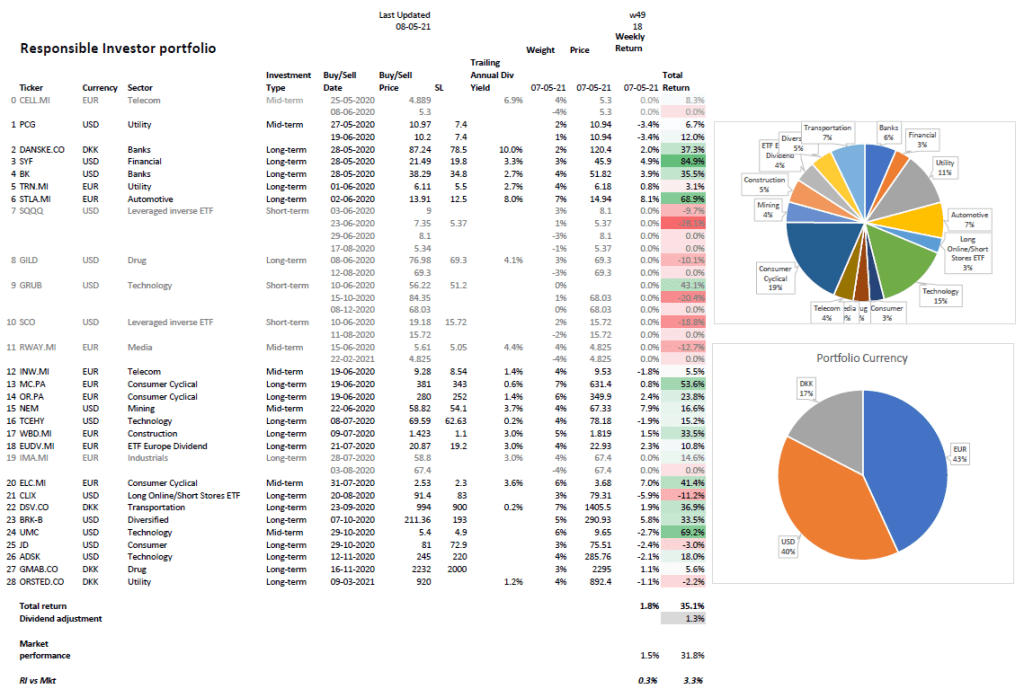

Our Responsible Investor portfolio is now up 35.1% (36.4% including dividends) in 49 weeks and is beating the market by 3.3% over the same period. We are about 64% in stocks & ETFs and 36% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.