The Big Picture

Even though inauguration day is not until next Wednesday, it really feels like this past week has been the first week of office for President-elect Joe Biden: it started with the House voting in favour of impeaching Trump following the violent events from the previous week and it continued with the prospect of a 1.9 trillion USD stimulus bill announced by Biden on Thursday which was a slight disappointment though it still came within the expected range. It is noted that this is the first of two stimulus interventions with the second one currently planned for the month of February.

As the number of available vaccines multiplies the attention is shifting towards how quickly they can be roll-out to achieve herd immunity. So far expectations remain unmet in most countries with Israel and Denmark representing notable exceptions. Biden has committed to achieving 100 million vaccinations in his first 100 days in office. The general sentiment is that despite this week’s retracement the bull market remains intact: investors will need to keep watching the vaccination roll-out to be on top of an environment very sensitive to negative news. The J&J vaccine is believed to play a key role in the roll-out as it belongs to the traditional kind and only requires a single shot, an important advantage especially in developing countries.

Market Performance

All indices were down this week: in the US the Nasdaq lost 1.6%, followed by the S&P500 (-1.5%) and the Dow (-0.9%). The Stoxx finished lower (-0.7%) and so did the Italian index (-1.8%) which was affected by the looming possibility of a change of government. The Danish OMX20 erased the gains of last week and finished 1.7% lower. The US Dollar gained 1.2% on the Euro as technical analysts see increasing signs of relative strength after loosing about 10% in 2020. Crude oil and $Gold finished higher. $BTC-USD had a rollercoaster week and lost 9.6% of its value.

Earnings

A few large US banks released their earnings on Friday: while all of them beat earnings they finished lower after the announcements. $JPM stood out and $WFC underwhelmed. $KBH beat earnings on Tuesday: I like the stock and own it in another portfolio.

In corporate news, our Danish drug/biotech $GMAB received $40M milestone payment in AbbVie collaboration and shot up 5.8% this week. The stock remains grossly undervalued and poised for more growth.

Next week more bank earnings are due, including $BK which we own, as well as $NFLX, $PG and $INTC among others.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend. Most Italian stocks traditionally pay dividend in late May, while US stocks distribute quarterly dividends.

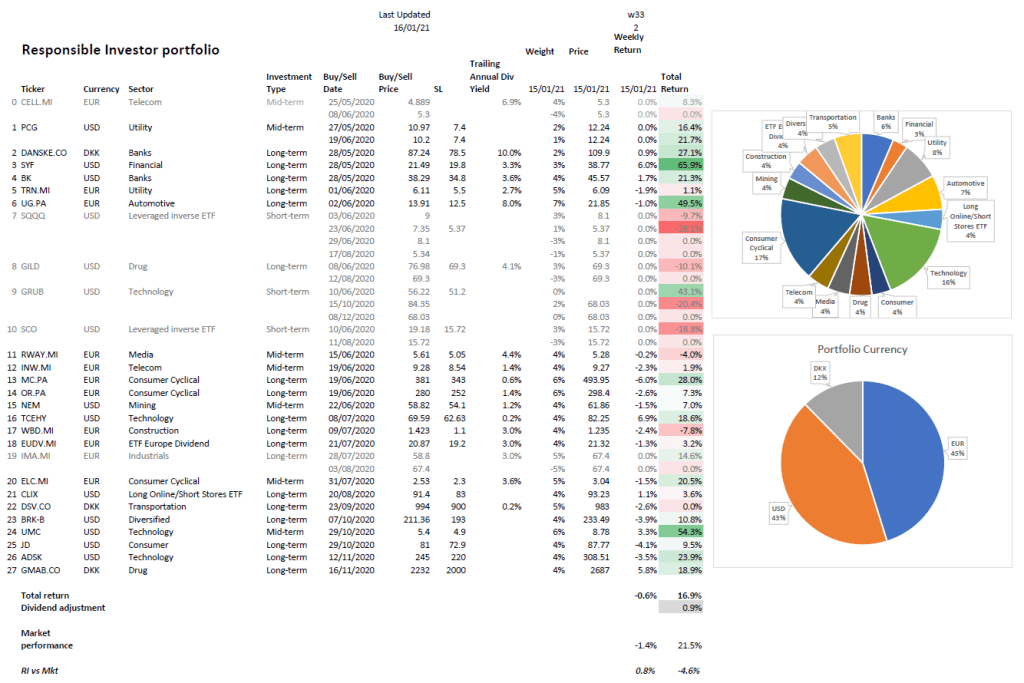

Portfolio Performance

Our portfolio down up 0.6% whereas the weighted average of the relevant market indices finished 1.4% lower, which means we have beaten the market this week (+0.8%).

It was another great week for our financial and fin-tech stocks: $SYF gained 6% and $BK added 1.7%. $TCEHY keeps pushing higher and gained 6.9%. $UMC added 3.3% and is now up 54% since we bought it. $MC.PA retraced 6%.

Our Responsible Investor portfolio is now up 16.9% (17.8% including dividends) in 33 weeks. We are about 58% in stocks & ETFs and 42% in cash. On my watchlist this week I have $DVA, $CMG, $AVGO, $LMND, $TRYG.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.