The Big Picture

The 10-year treasuries experienced a nominal decline this week which may signify a stabilisation after the sharp ascent of recent weeks. No incremental news were published on the fiscal policy and the Fed announced the lifting on capital returns restrictions (dividend and buybacks) from Q3.

The 3 trillion dollar infrastructure plan was announced by Biden on Wednesday although more information is expected next week. This stimulus package may offer great investment opportunities in the construction industry over the coming months.

Vaccine rollout optimism continues in the US although the daily vaccinations are unchanged at 2.5 million doses. Credit card data are already picking up more sales traffic as the re-opening play continues. The situation is more controversial in Europe where lockdowns persist, albeit inconsistently across the various countries, and vaccinations are still affected by pharma companies not being able to meet demand or deliver to the agreements.

Next week’s focus will be on the March US jobs report.

Market Performance

The stock market indices were mixed this week: in the US the Dow gained 1.4%, while the Nasdaq fell for the second week (-0.6%) and the S&P500 finished 1.6% higher. In Europe, the Stoxx and the Italian index rose by 0.8%. The Danish OMX20 finished flat. The US Dollar continues to gain over the Euro (0.8%). Crude $oil finished lower (-5%) despite the Suez canal blockage and so did $Gold (-0.4%). $BTC-USD experienced another decline this week (-5.6%).

Earnings

Three of our stocks reported their Q4 earnings last week. $TCEHY reported an earnings and a revenue beat but is believed to be the next target of Chinese regulators which might trigger more weakness after last month’s decline.

$WBD.MI announced their 2020 results and their intention of completing the purchase of Astaldi. Their better-than-expected debt and dividend increase surprised and pushed the stock price 6% higher on Monday.

$TRN.MI presented their 2020 consolidated results on Wednesday. Italy’s TSO beat on both the top and the bottom line and confirmed its 2021 guidance.

Notable earnings included $ADBE which reported record quarterly sales (+27%) and EPS up 38%, and high-end home improvement company $RH which smashed earnings expectations and is poised for more growth despite having already gained 430% over the last year.

All of our stocks have reported Q4 earnings now. The Q1 2021 earnings season will commence in three weeks’ time.

Dividends

Our Danish stock paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

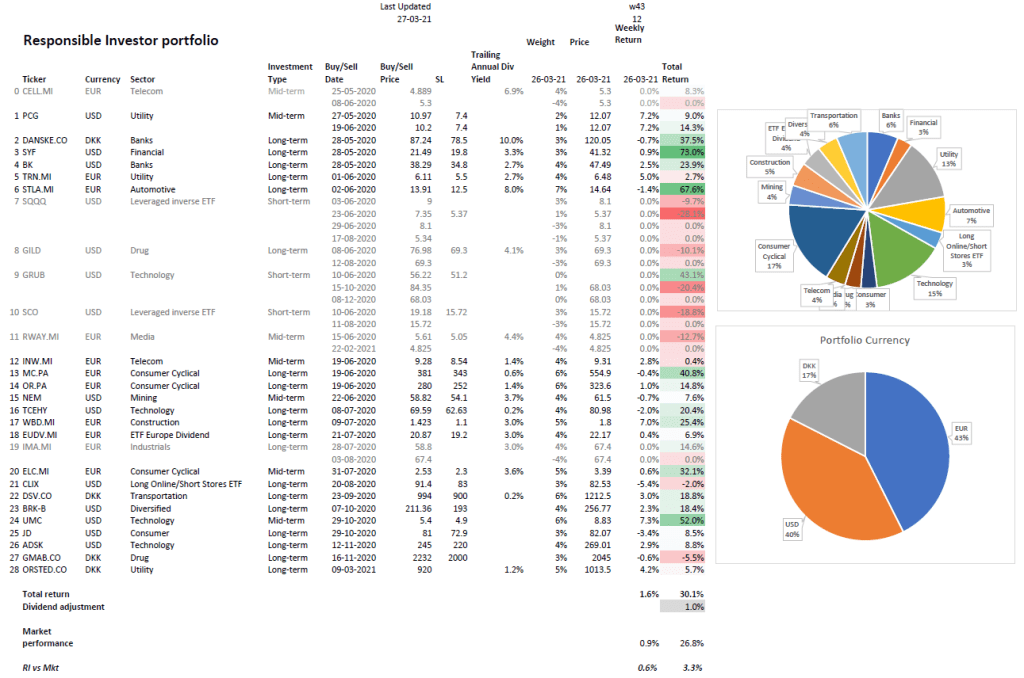

Portfolio Performance

Our portfolio gained 1.6% this week whereas the weighted average of the relevant market indices finished 0.9% higher, corresponding to a 0.7% market beat.

This week’s winner was $UMC with a 7.3% gain thanks to renewed strength in the semiconductor sector. Our energy stocks also finished markedly higher and so did the two Italian positions which reported Q4 earnings.

Our Responsible Investor portfolio is now up 30.1% (31.1% including dividends) in 43 weeks and is beating the market by 3.3% over the same period. We are about 60% in stocks & ETFs and 40% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.