The Big Picture

The markets were down this week as the rising 10-year treasuries spooked investors who are concerned that if the uptrend continues it might induce a pull back on the stock market. The counter-argument is that raising interest rates are caused by inflation which would be indicative of a solid economy. The covid-19 stimulus package is expected in March. Q4 earnings have mostly beat expectations and a few additional ones are due to be published over the next couple of weeks.

Vaccine news were mixed: on the negative news front, a US study showed that the $PFE vaccine is less effective on the south-African variant; on the flipside, data from Israel suggests that the effectiveness of the Pfizer vaccine is not impaired by lengthening the time between two doses which would increase the number of people who could get the first jab.

Market Performance

Most indices finished lower this week: in the US the Nasdaq led with a 1.6% loss, followed by the S&P500 (-0.9%) while the Dow was marginally higher (+0.1%). The Stoxx gained a meager 0.2% while the Italian index retraced -1.2%. The Danish OMX20 fell 1.1%. The US Dollar was unchanged relative to the Euro. Crude $oil retraced 0.5% and $Gold finished 2.2% lower. $BTC-USD gained 12% as the cryptocurrency flies past the 50k$ mark.

Earnings

$NEM reported a Q4 earnings beat this week as gold price rose and despite a reduction in gold production in its mines. The EPS more than doubled from the same quarter in the prior year with in-line income; the company guided higher on the basis of projected output and hiked the dividend from 0.4$/share to 0.55$/share which corresponds to a 3.81% forward yield.

$BRK-B latest 13F filing revealed the most recent changes in stake in the company positions including important divestments (eg $PFE and $JPM) and new holdings (eg $VZ and $CVX).

Notable earnings this week included $DE who crushed expectations and gained 9.9% on the news and $WMT who underwhelmed despite a good quarter and a stable outlook and slid 6.6%.

Returning to our portfolio, next week $PCG, $ADSK, $GMAB.CO and $BRK-B will report their Q4 earnings.

Dividends

$SYF paid its quarterly dividend on February 16th. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay an annual dividend in late May and US stocks distribute quarterly dividends.

Portfolio Performance

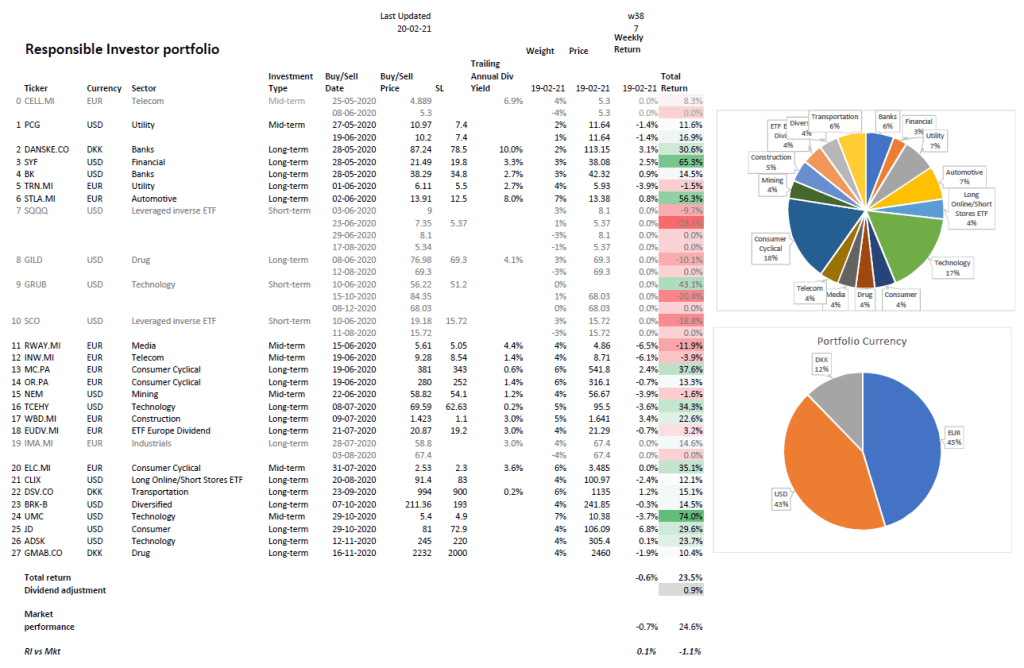

Our portfolio retraced 0.6% this week whereas the weighted average of the relevant market indices finished 0.7% lower which means that we beat the market by 0.1%.

Among this week’s winner we had $JD (+6.8%) and $DANSKE.CO (+3.1%). Two of our Italian stocks, $RWAY.MI and $INW.MI finished 6% lower, whereas $WBD.MI gained 3.4%.

Our Responsible Investor portfolio is now up 23.5% (24.4% including dividends) in 38 weeks. We are about 60% in stocks & ETFs and 40% in cash. On my watchlist this week I have $NIO, $CMG, $WMT, $MSFT, $AMBU-B.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.