Buy Ørsted A/S (ticker: $ORSTED.CO) with SL and TP to follow.

This is a long term investment opportunity in a large-cap green energy company for consideration: invest responsibly!

Invest in an aware, ethical and sustainable way

Buy Ørsted A/S (ticker: $ORSTED.CO) with SL and TP to follow.

This is a long term investment opportunity in a large-cap green energy company for consideration: invest responsibly!

The Big Picture

Despite the intra-day rally on Friday, the Nasdaq finished 2% lower this week as the technology sector was affected by a general sell-off in favour of value stocks. The energy sector was this week’s winner following the Opec + meeting which basically left production cuts unchanged and sustained the rally in crude oil. Only time will tell if the rotation will continue. Now more than ever is important to have a well diversified portfolio.

The 10-year treasuries reached 1.56% this week: the interest rates are up 60 basis points over the last 13 weeks. During an interview with the WSP on Thursday, chair Powell did not appear concerned with the rising interest rates given the general state of the economy – the markets did not react well to this analysis.

The 1.9 trillion $ stimulus is expected to be approved by the Senate this weekend ahead of President Biden signing it into bill next week. Attention will soon shift to the infrastructure package. The jobs reports exceeded expectations with most of new employments coming from the re-opening of bars, cafes and restaurants in the US. The unemployment rate has reached the lowest percentage since the pandemic begun.

On the covid front the positive vaccine data are balanced with the flattening of the infections, hospitalisations and deaths curves which may be due to factors such as relaxed behaviours and the impact of more contagious variants. In Europe the infection rates are on the rise again, paving the way to a possible third wave.

Market Performance

The stock market indices were mixed this week: in the US the Nasdaq fell 2.1%, whereas the S&P500 gained 0.8% and the Dow rose 1.8%. In Europe, the Stoxx gained 0.9% while the Italian index rose +0.5%. The Danish OMX20 fell for the third consecutive week (-3.9%). The US Dollar finished 1.4% stronger relative to the Euro. Crude $oil gained 9.9% while $Gold lost 2.2%. $BTC-USD finished 8.5% higher.

Earnings

Italy-based telecom company INW.MI reported Q4 earnings this week. The company announced an increase of EBITDA by 82% and confirmed guidance as outlook remains positive. The stock’s recent weakness is probably due to portfolio rotation into cyclical stock and to a rising interest environment, not to its fundamentals which remain intact.

Notable earnings this week included $ZM, who crushed expectations and posted a 370% revenue growth yoy, and $AVGO who beat both on earnings and revenue and confirmed their annual dividend at 3.24% which is significant given the companies growth rate.

Returning to our portfolio, next week $JD will report their Q4 earnings.

Dividends

Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay an annual dividend in late May and US stocks distribute quarterly dividends.

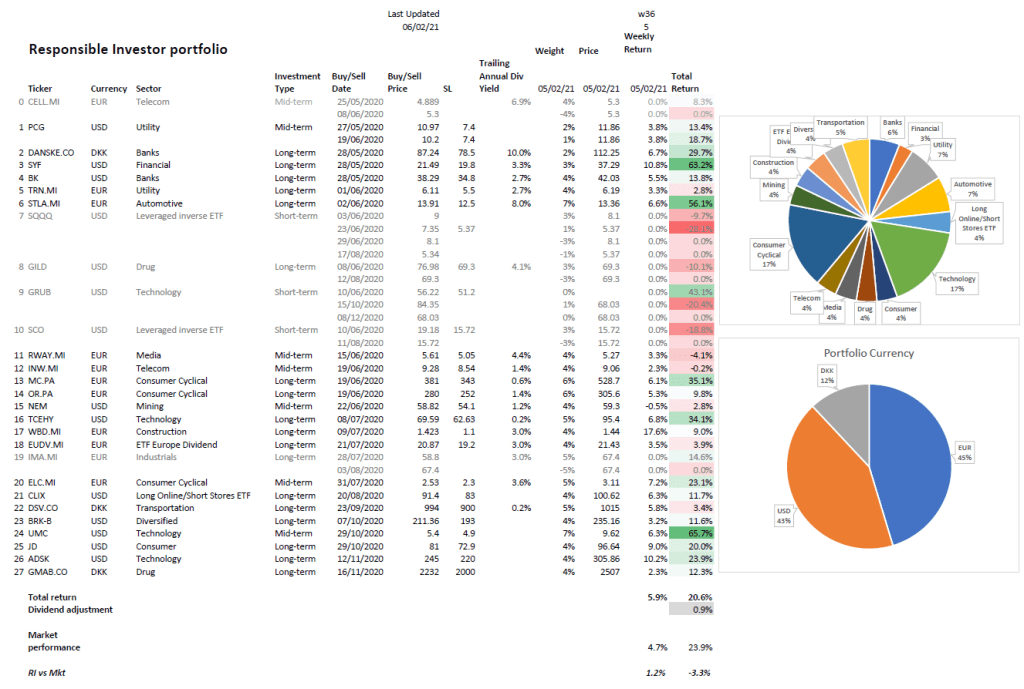

Portfolio Performance

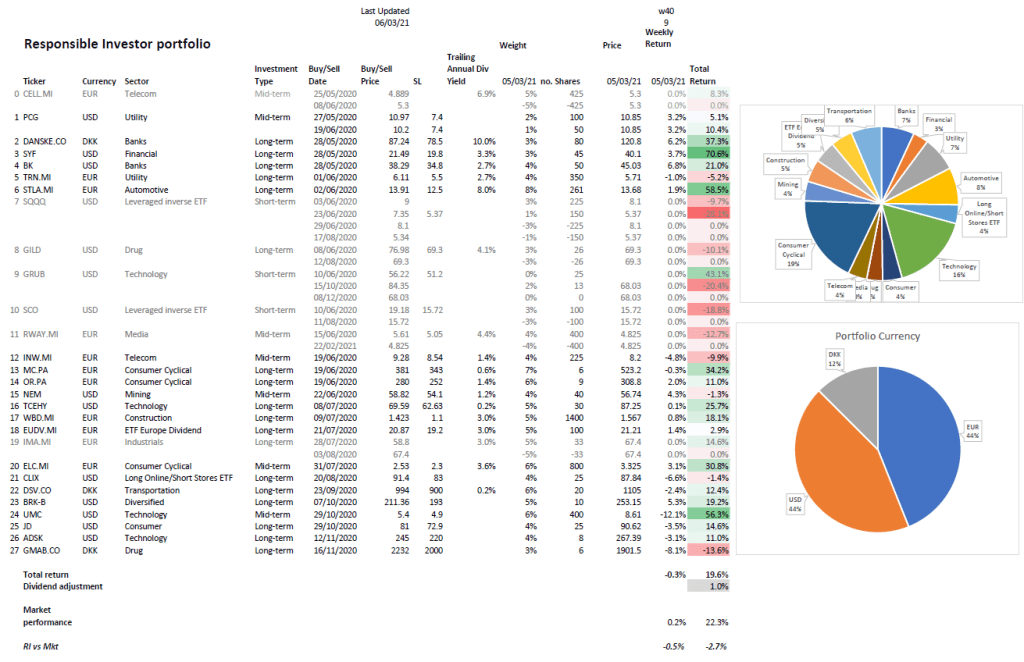

Our portfolio fell 0.3% this week whereas the weighted average of the relevant market indices finished 0.2 higher.

The tech stocks in our portfolio continued to be under pressure due to the market rotation but the rise of the financial and real economy stocks balanced the weekly performance.

Our Responsible Investor portfolio is now up 19.6% (20.6% including dividends) in 10 months. We are about 55% in stocks & ETFs and 45% in cash. On my watchlist this week I have $WMT, $MSFT, $AMBU-B.CO, $ABNB and $AVGO.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

The 10-year treasuries reached 1.5% this week, a level not seen since prior to the pandemic: the rising bond yields are believed to have caused the general sell off on the stock market, particularly for tech companies, even though the Nasdaq is still up more than 3% year to date. Consumer discretionary also lagged, while financials were flat, and energy came out as the best sector.

The 1.9 trillion $ stimulus was approved by the House yesterday but the Senate is likely to strip the 15$ minimum wage off the package. The next stimulus deal on the agenda is the infrastructure package which has bipartisan support except for the quantum.

Vaccine data keeps improving with the trendline of fewer infections, hospitalisations and deaths continuing. The vaccine rollout has now surpassed the 50 million doses mark which corresponds to half of the doses Biden promised to achieve in the first 100 days of office.

Market Performance

All indices finished lower this week: in the US the Nasdaq led with a 4.9% loss, followed by the S&P500 (-2.5%) and the Dow (-1.8%). In Europe, the Stoxx lost 2.4% while the Italian index retraced -1.2%. The Danish OMX20 fell 4.2%. The US Dollar was unchanged relative to the Euro. Crude $oil gained 7% and $Gold finished flat. $BTC-USD traded lower at 48k$ from the 57k$ level achieved last weekend.

Earnings

Four stocks of our portfolio reported Q4 earnings this week.

$BRK-B published their 2020 annual report on Wednesday and their Q4 earnings today (Saturday). In the annual letter to his shareholders Warren Buffett focused on operating margin, intrinsic value, and buy-backs. The company hasn’t made sizeable acquisitions in 2020 and has recently sold some $AAPL shares and increased the stake in value companies. The stock was marginally down this week.

$ADSK beat on both the top and the bottom line on Thursday but guided lower which led to a sharp decline, partly caused by the general weakness in the technology sector. The strong Q4 earnings were offset by revenue and EPS expectations below consensus.

$PCG reported a marginal earnings beat on Thursday, though revenue fell short. The company reaffirmed its 2021 guidance. The market did not react well and the stock fell by 9% and underperformed compared to the energy sector stocks.

$GMAB.CO reported Q4 earnings on Tuesday, with a revenue beat thanks to an 88% increase year on year. The Danish biotech company also reported operating profit above expectations and initiated a share buy-back programme.

Notable earnings this week included $NVDA, who smashed expectations, and $ABNB who missed on earnings but beat on revenue and has the prospect of restrictions lift which are expected to lead to a significant travel rebound..

Returning to our portfolio, next week $INW.MI will report their Q4 earnings.

Dividends

Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay an annual dividend in late May and US stocks distribute quarterly dividends.

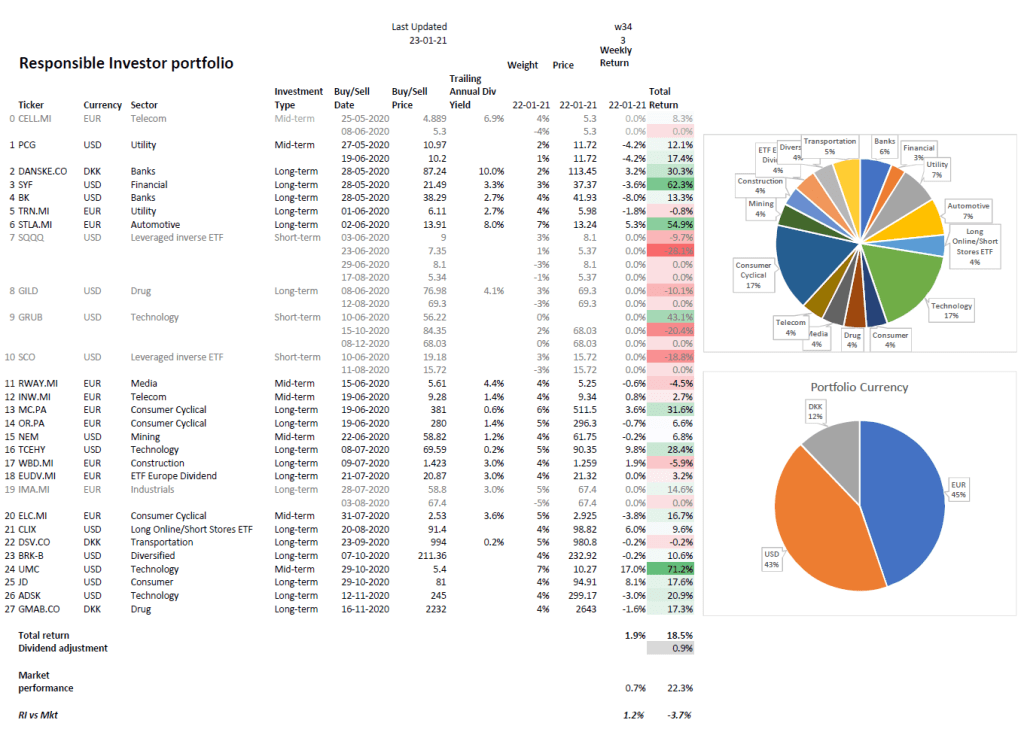

Portfolio Performance

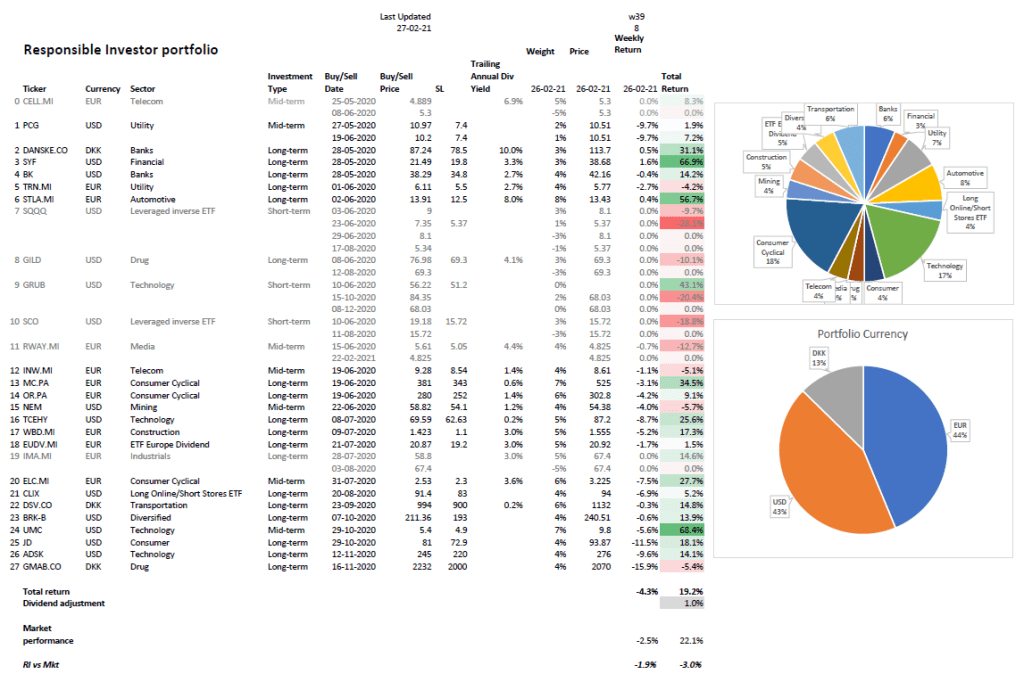

Our portfolio fell 4.3% this week whereas the weighted average of the relevant market indices finished 2.5 lower.

We exited our position in $RWAY.MI on Monday as the stock showed more signs of weakness after the previous week’s sell-off. Technically, the stock has also fallen below the 38.2 fib which could have led to further downward action. Our tech stocks were hit by the sector weakness but their fundamentals remain intact. The only positive performance was that of $SYF which finished 1.6% higher and is now up 67% since we bought it.

Our Responsible Investor portfolio is now up 19.2% (20.2% including dividends) in 39 weeks. We raised same cash this week and are about 55% in stocks & ETFs and 45% in cash. On my watchlist this week I have $WMT, $MSFT, $AMBU-B.CO, $ABNB and $SQ.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

The markets were down this week as the rising 10-year treasuries spooked investors who are concerned that if the uptrend continues it might induce a pull back on the stock market. The counter-argument is that raising interest rates are caused by inflation which would be indicative of a solid economy. The covid-19 stimulus package is expected in March. Q4 earnings have mostly beat expectations and a few additional ones are due to be published over the next couple of weeks.

Vaccine news were mixed: on the negative news front, a US study showed that the $PFE vaccine is less effective on the south-African variant; on the flipside, data from Israel suggests that the effectiveness of the Pfizer vaccine is not impaired by lengthening the time between two doses which would increase the number of people who could get the first jab.

Market Performance

Most indices finished lower this week: in the US the Nasdaq led with a 1.6% loss, followed by the S&P500 (-0.9%) while the Dow was marginally higher (+0.1%). The Stoxx gained a meager 0.2% while the Italian index retraced -1.2%. The Danish OMX20 fell 1.1%. The US Dollar was unchanged relative to the Euro. Crude $oil retraced 0.5% and $Gold finished 2.2% lower. $BTC-USD gained 12% as the cryptocurrency flies past the 50k$ mark.

Earnings

$NEM reported a Q4 earnings beat this week as gold price rose and despite a reduction in gold production in its mines. The EPS more than doubled from the same quarter in the prior year with in-line income; the company guided higher on the basis of projected output and hiked the dividend from 0.4$/share to 0.55$/share which corresponds to a 3.81% forward yield.

$BRK-B latest 13F filing revealed the most recent changes in stake in the company positions including important divestments (eg $PFE and $JPM) and new holdings (eg $VZ and $CVX).

Notable earnings this week included $DE who crushed expectations and gained 9.9% on the news and $WMT who underwhelmed despite a good quarter and a stable outlook and slid 6.6%.

Returning to our portfolio, next week $PCG, $ADSK, $GMAB.CO and $BRK-B will report their Q4 earnings.

Dividends

$SYF paid its quarterly dividend on February 16th. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay an annual dividend in late May and US stocks distribute quarterly dividends.

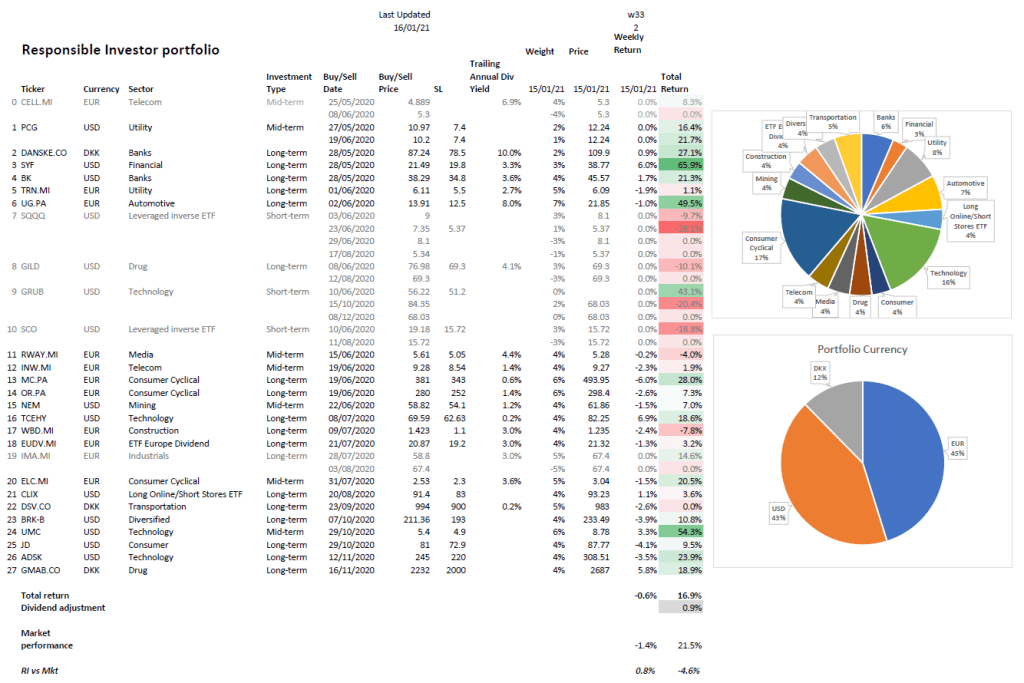

Portfolio Performance

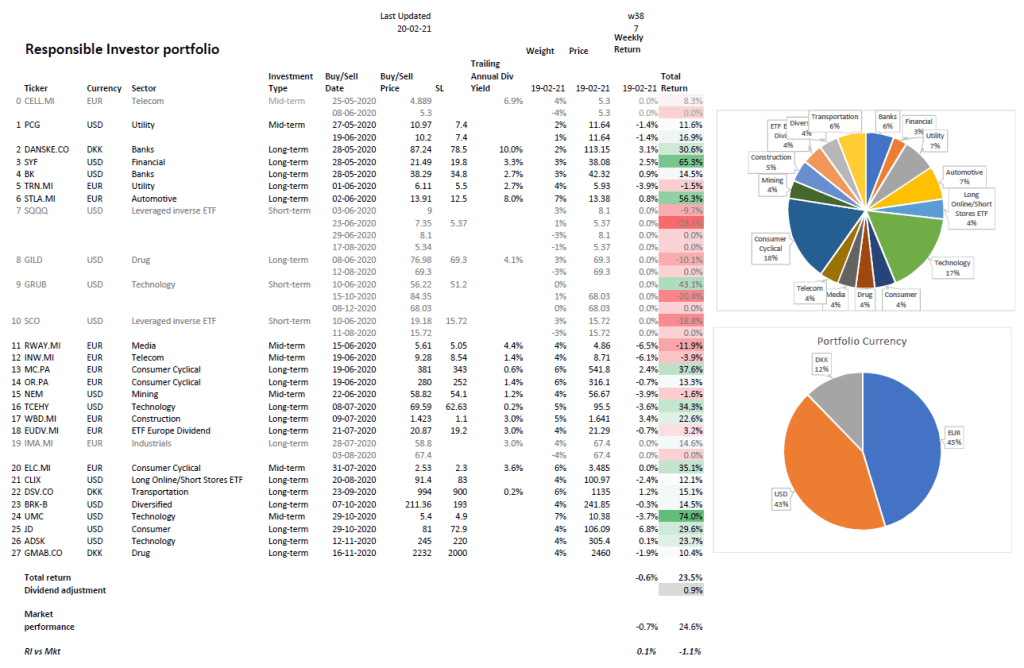

Our portfolio retraced 0.6% this week whereas the weighted average of the relevant market indices finished 0.7% lower which means that we beat the market by 0.1%.

Among this week’s winner we had $JD (+6.8%) and $DANSKE.CO (+3.1%). Two of our Italian stocks, $RWAY.MI and $INW.MI finished 6% lower, whereas $WBD.MI gained 3.4%.

Our Responsible Investor portfolio is now up 23.5% (24.4% including dividends) in 38 weeks. We are about 60% in stocks & ETFs and 40% in cash. On my watchlist this week I have $NIO, $CMG, $WMT, $MSFT, $AMBU-B.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

It was a rather uneventful week with most indices finishing with moderate gains. After months of headlines dominated by the US presidential election, Brexit and rising Covid-19 numbers, the narrative seems to lack negative arguments and the bulls thrive. Record high debt and prolonged borrowing does not appear to be of concern for the markets which find their support on the tripod consisting of earnings beats, stimulus bill and positive vaccine news. The employment numbers published this week were mostly in-line and almost ignored, however next week the calendar features data which could affect the markets.

Market Performance

All indices finished higher this week: in the US the Nasdaq led with a 1.7% gain, followed by the S&P500 (+1.5%) and the Dow (+1.0%). The Stoxx gained 1.1% and the Italian index keeps ascending (+1.4%) as Mario Draghi’s new government is sworn in today. The Danish OMX20 finished 1.8% higher. The US Dollar gained 0.6% on the Euro. Crude oil is now back to pre-Covid levels and $Gold finished 0.8% higher. $BTC-USD shot to the upside by 23% following the controversial announcement by Elon Musk about $TSLA investing 1.5 billion USD in the cryptocurrency.

Earnings

Three stocks of our portfolio reported earning this week.

$DSV.CO reported Q4 earnings on February 12th with a revenue beat and in-line EBIT. The company declared a 4 DKK dividend for 2020 which corresponds to 0.35% yield at today’s price level. The stock gained 10.4% this week due to these results and the positive outlook.

$OR.PA announced the 2020 results this week. The company reported revenues of 28 billion € and operating profit of 18.6%. The e-commerce revenues increased by 62% and the annual dividend has been set at 4€ per share. The outlook remains positive with a projected growth of 4.8% in Q1 2021 despite market volatility and uncertainty.

$ELC.MI reported the Q4 earnings and the preliminary 2020 results. While the company has seen a decline of sales with respect to the previous year, the Q4 revenue was up 15% relative to Q3 driven by its cooking segment. The stock was up 12.1% this week and 35% overall since we bought it.

Notable earnings this week included $DIS who beat expectations and announced more than 90 million Disney+ subscribers, a threshold that only 9 months ago they were expecting to reach no sooner than in 2023.

Returning to our portfolio, $NEM will report their Q4 earnings next week.

Dividends

$SYF went ex-dividend last week, the quarterly dividend is payable on February 16th. The quarterly dividend for $BK was paid on Friday. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay a dividend in late May and US stocks distribute quarterly dividends.

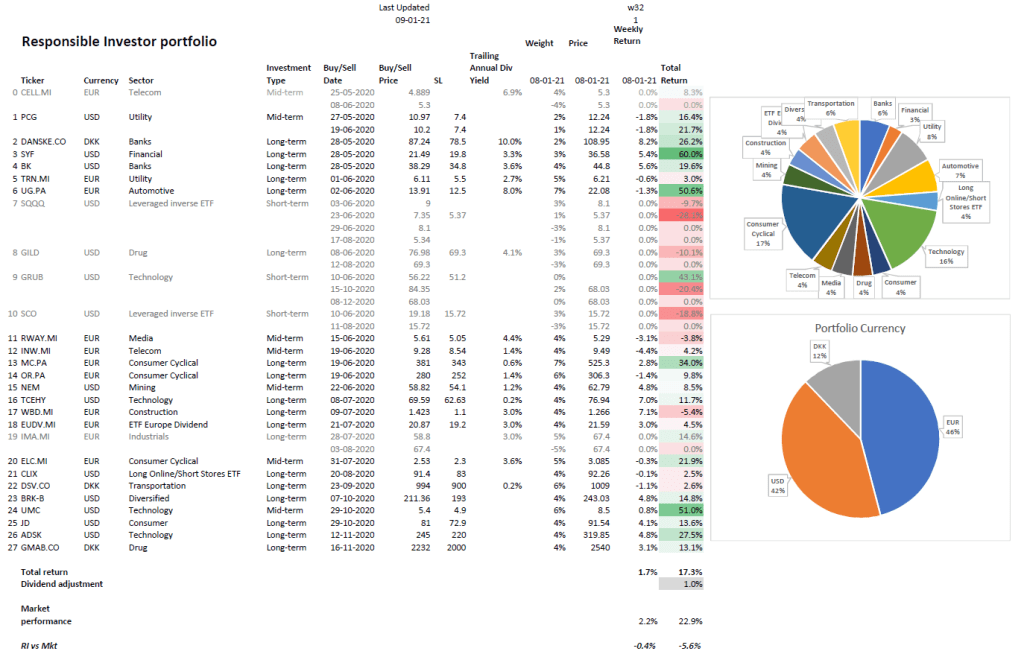

Portfolio Performance

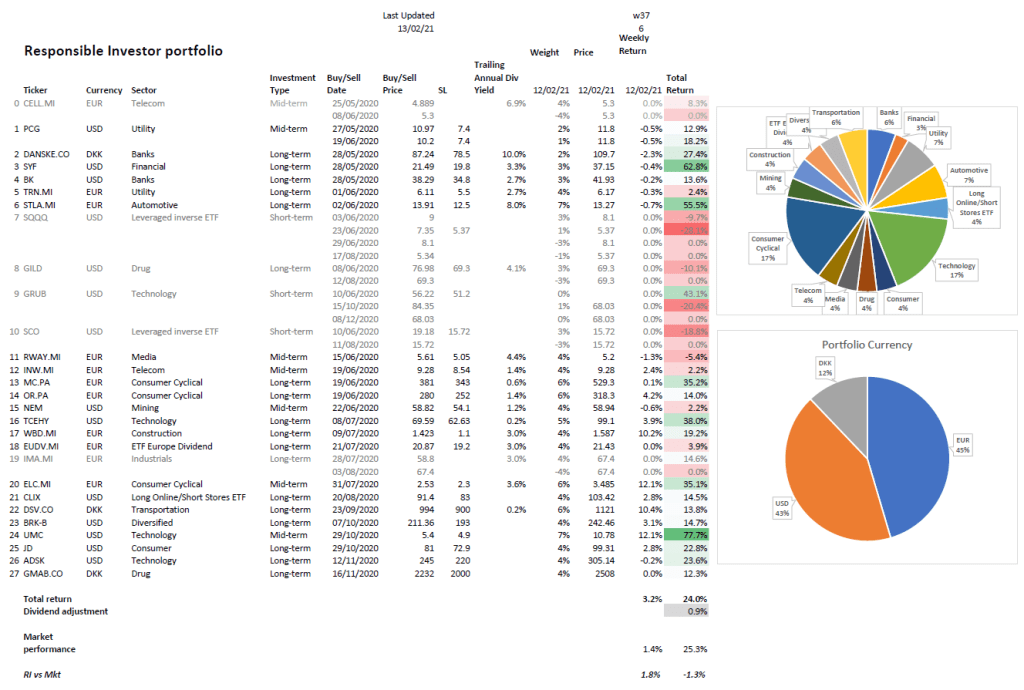

Our portfolio gained 3.2% this week whereas the weighted average of the relevant market indices finished 1.4% higher which means that we beat the market by 1.8%.

$WBD.MI gained more than 10% supported by the prospect of infrastructure investment in Italy thanks to the the EU Recovery Fund. $UMC had another great week with a 12% gain – the stock is up 77% in less than 4 months.

Our Responsible Investor portfolio is now up 24.0% (24.9% including dividends) in 37 weeks. We are about 61% in stocks & ETFs and 39% in cash. On my watchlist this week I have $NIO, $CMG, $VIAV, $MSFT, $AMBU-B.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

Last week’s drop already seems like a distant memory as the markets field significant gains this week with some indices reaching new all time highs. There is an inherent inconsistency between the stocks, the dollar and the treasuries all going up at the same time, however: at some point something has got to give. Positive Q4 earnings keep pouring in and negotiations for the stimulus bill continue. On the vaccine front, the $JNJ vaccine continues to attract attention and reports postulate that preventative measures as well as vaccinations start to reduce infection rates and hospitalisations.

Market Performance

All indices finished higher this week: in the US the Nasdaq led with a 6.0% gain, followed by the S&P500 (+4.7%) and the Dow (+3.9%). The Stoxx gained 3.4% and the Italian index gapped 7.0% higher as Mario Draghi accepted the task to form a new government. The Danish OMX20 finished 3.9% higher. The US Dollar gained 0.7% on the Euro. Crude oil was markedly higher while $Gold finished 1.6% lower. $BTC-USD gained more than 10% continuing its recovery from the sharp January fall.

Earnings

One of our stocks reported Q4 earnings this week. $DANSKE.CO presented its 2020 annual report on Thursday and the results were in-line. The Danish bank continues on its journey to increase its profitability after the money laundering scandal that hit it a few years ago. The stock was up 6.7% this week.

Notable earnings this week included $AMZN and $GOOG who beat on both the top and the bottom line by a wide margin. The e-commerce and cloud service giant also announced Jeff Bezos stepping down as CEO and passing the baton to the executive in charge of AWS – Amazon’s profit machine.

Next week two of our stocks will report their earnings: $DSV.CO and $OR.PA.

Dividends

$BK went ex-dividend last week, the quarterly dividend is payable on February 12th. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay a dividend in late May and US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 5.9% this week whereas the weighted average of the relevant market indices finished 4.7% higher which means that we beat the market by 1.2%.

$WBD.MI jumped 17.6% and is now in the black for the first time since we purchased it. $ADSK gained 10.2% after three consecutive weeks of decline. $SYF rose 10.8% thereby erasing the loss from the previous week.

Our Responsible Investor portfolio is now up 20.6% (21.5% including dividends) in 9 months. We are about 60% in stocks & ETFs and 40% in cash. On my watchlist this week I have $DVA, $CMG, $VIAV, $MSFT, $AMBU-B.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

While hundreds of earnings were published this week reporting better than expected earnings, the narrative was dominated by the retail-driven short squeeze of a number of heavily shorted stocks. The volatility that ensued resulted in two steep declines on Wednesday and Friday which sent the US stock markets more than 3% down. Some labelled this as a battle between generations or ‘classes’ of investors: to be honest it seems more like irresponsible investing and a failure of the stock market regulators to me.

Despite this decline, however, the bullish sentiment seems intact and supported by the ‘tripod’ consisting of positive earnings, vaccine optimism and the forthcoming stimulus bill. There were several positive vaccine news this week: $NVAX reported 89% efficacy in the UK trials and 60% in South Africa, the EMA approved the $AZN vaccine in Europe and $JNJ stated that their vaccine is 66% effective. This latter news initially underwhelmed but it is actually more positive than one would think at first look especially given the fact that it only requires a single shot.

Market Performance

All US indices were markedly down this week: in the US the Nasdaq led with a 3.5% decline, followed by the S&P500 and the Dow which both lost 3.3% of their value. The Stoxx fell 3.1% and the Italian index contained the loss to 2.3% as the political crisis sees a mildly positive optimism. The Danish OMX20 dropped 4.3%. The US Dollar gained 0.3% on the Euro. Crude oil was softer and $Gold finished 0.5% lower. $BTC-USD gained 3.3% after two consecutive weeks of sharp declines.

Earnings

Three of our stocks reported Q4 earnings this week. $MC.PA rose 1.3% on Wednesday after beating expectations with sales rising 18% year-on-year on a comparable basis.

$UMC missed on revenue despite an 8.2% yoy growth, while EPS rose to 0.16$ from 0.13$ in Q3. Their foundries are now at 99% capacity and the company guided in line. The stock sell off and underperformed relative to the Nasdaq this week: it is still up 59.4% since we initiated our position, however.

$SYF crushed earnings on Friday with Q4 EPS of 1.24$ vs consensus estimate of 0.85$ and improved from 0.52$ of Q3. Despite gaining in pre-market, the stock sell-off with the rest of the market that day which could provide an opportunity for accumulation in the near future.

Other notable earnings included $AAPL who beat expectations, and $MSFT whose cloud revenues grew 34% year on year. In the physical world, $CAT beat earnings despite a revenue fall.

Next week $DANSKE.CO will present its 2020 annual report.

Dividends

$BK went ex-dividend this week, the quarterly dividend is payable on February 12th. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay a dividend in late May and US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio fell 4.2% whereas the weighted average of the relevant market indices finished 3.1% lower.

Our Responsible Investor portfolio is now up 14.5% (15.5% including dividends) in 35 weeks. We are about 56% in stocks & ETFs and 44% in cash. On my watchlist this week I have $DVA, $CMG, $VIAV, $MSFT, $TRYG.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

The 46th US President inauguration was an uplifting ceremony which made history on many levels. The next 100 days will be key to appreciate the direction this administration will take. In his first days in office Biden signed a flurry of executive orders to dismantle several policies which were set in place by his predecessor.

Meanwhile the US markets continued to rally, especially the Nasdaq, off the back of positive Q4 earnings news, vaccine optimism and the prospect of the next stimulus bill. Scratching the surface, however, one finds several counter-arguments to this “risk on” environment: paradoxically, a significant growth in earnings could undermine the monetary expansion; vaccine roll-out is being affected by various glitches in doses delivery; and the negotiations for the stimulus bill are unlikely to result in a smooth ride for the new administration.

Market Performance

All US indices were up this week: in the US the Nasdaq led with a whopping 4.2%, followed by the S&P500 (1.9%) and the Dow (0.6%). The Stoxx finished flat while the Italian index lost 1.3% as uncertainty continues to affect its political environment. The Danish OMX20 gained 1.3%. The US Dollar lost 0.2% on the Euro. Crude oil was softer while $Gold finished 0.8% higher. $BTC-USD had another horrible week and lost 9.7% after the fall of the previous week.

Earnings

$BK beat Q4 earnings but the market did not react well and the stock finished 8% lower. We are still up 13.3% since we purchased it and will take action should there be any further signs of weakness.

Other notable earnings included $NFLX who crushed estimates and exceeded 200M subscribers for the first time and lukewarm Q4 results from $INTC.

Next week two of our stocks will report earnings, $UMC and $SYF, as well as many other well know companies such as $MSFT, $AAPL and $FB.

Dividends

$BK goes ex-dividend next week. Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay a dividend in late May and US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio was up 1.9% whereas the weighted average of the relevant market indices finished 0.7% higher, which means we have beaten the market this week (+1.2%).

$UMC jumped 17% this week and is now up 72% overall! $TCEHY was up 9.8% increasing the gain of the last 3 weeks to 24%. Our long e-commerce/short bricks and mortar ETF grew 6%. From this week we will start reporting $UG.PA under the new ticker $STLA.MI following the merger with FGA which resulted in the conversion of every Peugeout share into 1.742 shares of Stellantis: the European car maker had an excellent first week of trading finishing 5.3% higher.

Our Responsible Investor portfolio is now up 18.5% (19.4% including dividends) in 34 weeks. We are about 59% in stocks & ETFs and 41% in cash. On my watchlist this week I have $DVA, $CMG, $VIAV, $TRYG.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

Even though inauguration day is not until next Wednesday, it really feels like this past week has been the first week of office for President-elect Joe Biden: it started with the House voting in favour of impeaching Trump following the violent events from the previous week and it continued with the prospect of a 1.9 trillion USD stimulus bill announced by Biden on Thursday which was a slight disappointment though it still came within the expected range. It is noted that this is the first of two stimulus interventions with the second one currently planned for the month of February.

As the number of available vaccines multiplies the attention is shifting towards how quickly they can be roll-out to achieve herd immunity. So far expectations remain unmet in most countries with Israel and Denmark representing notable exceptions. Biden has committed to achieving 100 million vaccinations in his first 100 days in office. The general sentiment is that despite this week’s retracement the bull market remains intact: investors will need to keep watching the vaccination roll-out to be on top of an environment very sensitive to negative news. The J&J vaccine is believed to play a key role in the roll-out as it belongs to the traditional kind and only requires a single shot, an important advantage especially in developing countries.

Market Performance

All indices were down this week: in the US the Nasdaq lost 1.6%, followed by the S&P500 (-1.5%) and the Dow (-0.9%). The Stoxx finished lower (-0.7%) and so did the Italian index (-1.8%) which was affected by the looming possibility of a change of government. The Danish OMX20 erased the gains of last week and finished 1.7% lower. The US Dollar gained 1.2% on the Euro as technical analysts see increasing signs of relative strength after loosing about 10% in 2020. Crude oil and $Gold finished higher. $BTC-USD had a rollercoaster week and lost 9.6% of its value.

Earnings

A few large US banks released their earnings on Friday: while all of them beat earnings they finished lower after the announcements. $JPM stood out and $WFC underwhelmed. $KBH beat earnings on Tuesday: I like the stock and own it in another portfolio.

In corporate news, our Danish drug/biotech $GMAB received $40M milestone payment in AbbVie collaboration and shot up 5.8% this week. The stock remains grossly undervalued and poised for more growth.

Next week more bank earnings are due, including $BK which we own, as well as $NFLX, $PG and $INTC among others.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend. Most Italian stocks traditionally pay dividend in late May, while US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio down up 0.6% whereas the weighted average of the relevant market indices finished 1.4% lower, which means we have beaten the market this week (+0.8%).

It was another great week for our financial and fin-tech stocks: $SYF gained 6% and $BK added 1.7%. $TCEHY keeps pushing higher and gained 6.9%. $UMC added 3.3% and is now up 54% since we bought it. $MC.PA retraced 6%.

Our Responsible Investor portfolio is now up 16.9% (17.8% including dividends) in 33 weeks. We are about 58% in stocks & ETFs and 42% in cash. On my watchlist this week I have $DVA, $CMG, $AVGO, $LMND, $TRYG.CO and $OCDO.L.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The Big Picture

The disconnect between the physical world and the stock market was particularly evident this week as Wall Street rallied during the Capitol Hill insurrection. Stimulus and money printing continues to inflate the market and boost valuations. From that point of view, the outcome of the Georgia senate race in favour of the Democrats is believed to further increase borrowing and allow the ongoing reflation trade to continue. It is however considered unlikely that the razor thin majority that the Democrats will have in Congress will allow Biden’s administration to pass radical reforms, especially on the corporate tax side.

This week was the time of the Moderna vaccine approval in the UK and in Europe. The increase of doses that the various vaccines offer is helping the market retain a positive outlook for 2021 and beyond. The growing number of cases and deaths in the US as well as in the UK does not seem to cause significant concerns for investors who experienced an “everything rally” first week of trading in 2021. Studies and expert opinions about the efficacy of the vaccines on the new strains of Covid-19 keep coming in but do not steal the scene in the news cycles.

Market Performance

All indices were up this week: in the US the Nasdaq led with a 2.4% gain, followed by the Dow (+1.8%) and the S&P500 (+1.6%). The Stoxx rallied (+3.0%) and so did the Italian index (+2.5%) despite the possibility of a change of government. The Danish OMX20 finished 1.4% higher. The US Dollar lost ground relative to the Euro reversing the trend from the previous two weeks. Crude oil joined the markets in the rally while $Gold finished lower. $BTC-USD gained more than 30% in a single week and whizzed past the 423.6% fib.

Earnings

A handful of earnings were released this week. Notable ones include $BBBY and $CAG who missed expectations, and $STZ and $MU who beat on both the top and the bottom line.

In other corporate news, $FCA.MI and $UG.PA announced that they will begin trading under the ticker of the newly formed merger company Stellantis next week.

The earning season starts next week with the first batch of bank stocks.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend. Most Italian stocks traditionally pay dividend in late May, while US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio was up 1.7% whereas the weighted average of the relevant market indices finished 2.2% higher.

The financial stocks keep pushing higher: $SYF gained 5.4% and $DANSKE.CO jumped 8.2%; $BK added 5.6% and is now up 20% overall. Our Chinese stocks had a very good week with $TCEHY and $JD gaining 7% and 4.1%, respectively. There is an ongoing political battle between the US and China over Chinese stocks trading in the US which, while it has not affected our positions so far, needs to be watched closely.

Our Responsible Investor portfolio is now up 17.3% (18.3% including dividends) in 8 months. We are about 58% in stocks & ETFs and 42% in cash. On my watchlist this week I have $DVA, $CMG, $MA, $CRWD, $AVGO, $LMND, $TRYG.CO and $ADBE.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.