The Big Picture

Despite the intra-day rally on Friday, the Nasdaq finished 2% lower this week as the technology sector was affected by a general sell-off in favour of value stocks. The energy sector was this week’s winner following the Opec + meeting which basically left production cuts unchanged and sustained the rally in crude oil. Only time will tell if the rotation will continue. Now more than ever is important to have a well diversified portfolio.

The 10-year treasuries reached 1.56% this week: the interest rates are up 60 basis points over the last 13 weeks. During an interview with the WSP on Thursday, chair Powell did not appear concerned with the rising interest rates given the general state of the economy – the markets did not react well to this analysis.

The 1.9 trillion $ stimulus is expected to be approved by the Senate this weekend ahead of President Biden signing it into bill next week. Attention will soon shift to the infrastructure package. The jobs reports exceeded expectations with most of new employments coming from the re-opening of bars, cafes and restaurants in the US. The unemployment rate has reached the lowest percentage since the pandemic begun.

On the covid front the positive vaccine data are balanced with the flattening of the infections, hospitalisations and deaths curves which may be due to factors such as relaxed behaviours and the impact of more contagious variants. In Europe the infection rates are on the rise again, paving the way to a possible third wave.

Market Performance

The stock market indices were mixed this week: in the US the Nasdaq fell 2.1%, whereas the S&P500 gained 0.8% and the Dow rose 1.8%. In Europe, the Stoxx gained 0.9% while the Italian index rose +0.5%. The Danish OMX20 fell for the third consecutive week (-3.9%). The US Dollar finished 1.4% stronger relative to the Euro. Crude $oil gained 9.9% while $Gold lost 2.2%. $BTC-USD finished 8.5% higher.

Earnings

Italy-based telecom company INW.MI reported Q4 earnings this week. The company announced an increase of EBITDA by 82% and confirmed guidance as outlook remains positive. The stock’s recent weakness is probably due to portfolio rotation into cyclical stock and to a rising interest environment, not to its fundamentals which remain intact.

Notable earnings this week included $ZM, who crushed expectations and posted a 370% revenue growth yoy, and $AVGO who beat both on earnings and revenue and confirmed their annual dividend at 3.24% which is significant given the companies growth rate.

Returning to our portfolio, next week $JD will report their Q4 earnings.

Dividends

Most Danish companies go ex-dividend in March, while Italian stocks traditionally pay an annual dividend in late May and US stocks distribute quarterly dividends.

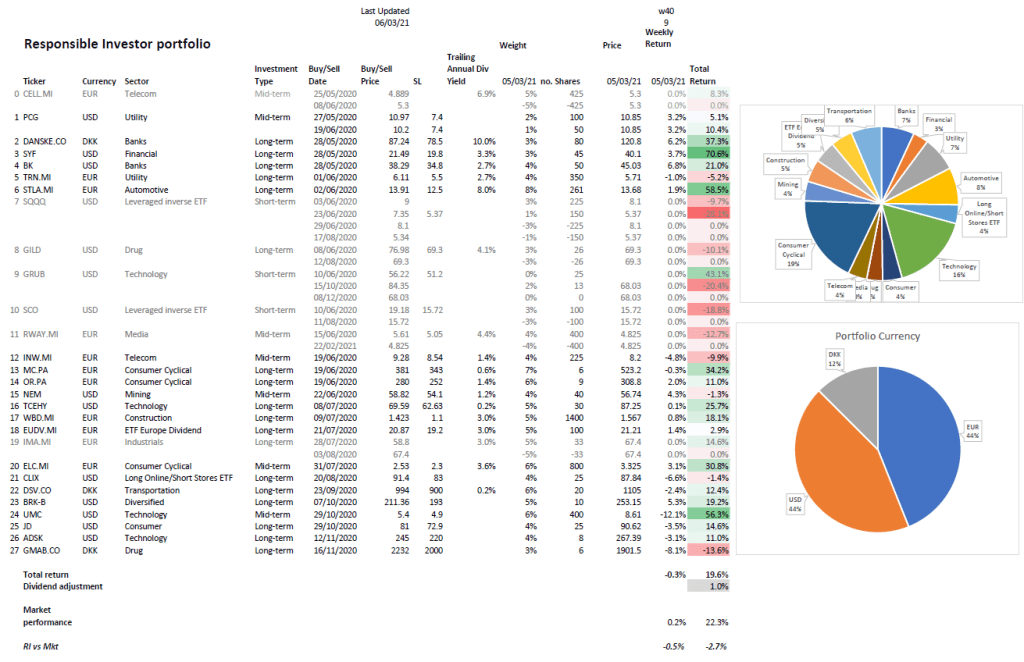

Portfolio Performance

Our portfolio fell 0.3% this week whereas the weighted average of the relevant market indices finished 0.2 higher.

The tech stocks in our portfolio continued to be under pressure due to the market rotation but the rise of the financial and real economy stocks balanced the weekly performance.

Our Responsible Investor portfolio is now up 19.6% (20.6% including dividends) in 10 months. We are about 55% in stocks & ETFs and 45% in cash. On my watchlist this week I have $WMT, $MSFT, $AMBU-B.CO, $ABNB and $AVGO.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.