The Big Picture

The Covid-19 numbers keep rising in the US and while good news on the vaccine front instill confidence in the future, the near term appears very challenging. The impression is that mitigation measures are not being implemented as quickly as they should in the US, whereas lockdowns are announced every day in Europe, especially considering the upcoming holiday season is seen as a clear threat. Negotiations on the stimulus bill continue and seems to be very close to a positive resolution which might come as early as next week.

After last week’s positive vote for the $PFE vaccine, the FDA advisory board gave the green light to the $MRNA vaccine on Friday with no votes cast against it. This emergency authorization will increase the distribution of the vaccine within the US population, especially since it requires much lower storage temperatures.

The Fed met for the last time in 2021 on Wednesday meeting. The FOMC statement was quite dovish and Powell expects growth to pick up in the second half of the year. Bond buying will continue at a clip of 120B $ per month for the foreseeable future. The injection of liquidity has been massive and is believed to have propped the market considerably in recent months. The excess liquidity in particular, ie the liquidity that is not absorbed by the economy, tends to grow valuations. Nobel-prize winner and Yale professor Robert Schiller stated that valuations are not excessive earlier this month. Earnings have deflated 15% globally in 2020 but the 25% liquidity increase caused by central banks has made the markets gain 10% on average. With earnings expected to increase again in 2021 the market should go higher and valuations become more reasonable.

Market Performance

All US market indices finished higher, led by the Nasdaq, up 3.1%, followed by the S&P500 (1.3%) and the Dow (0.4%). The Stoxx was also higher (1.5%) and the Italian index partly recovered from last week’s loss ending with a 1.3% gain. The Danish OMX20 rallied 4.1% and is lined up to be the best index in developed countries this year. The US Dollar fell relative to the Euro and gold finished higher.

Earnings

$ACN traditionally reports earlier than most stocks and beat Q1 earnings on Thursday before market open and guided higher for 2021. The stock jumped 7% on that day and reached all time highs. I like the stock a lot and continue to own it in another portfolio.

$FDX also reported an earnings beat this week with 19% growth of the top line and more than double EPS yoy. Clearly the company, alongside its peers, has benefitted from a sharp increase in e-commerce and shipping demand. The stock fell sharply, however, after not providing guidance for 2021.

Dividends

The next dividend payments for our stocks are due in March, which is when most Danish company go ex-dividend.

Portfolio Performance

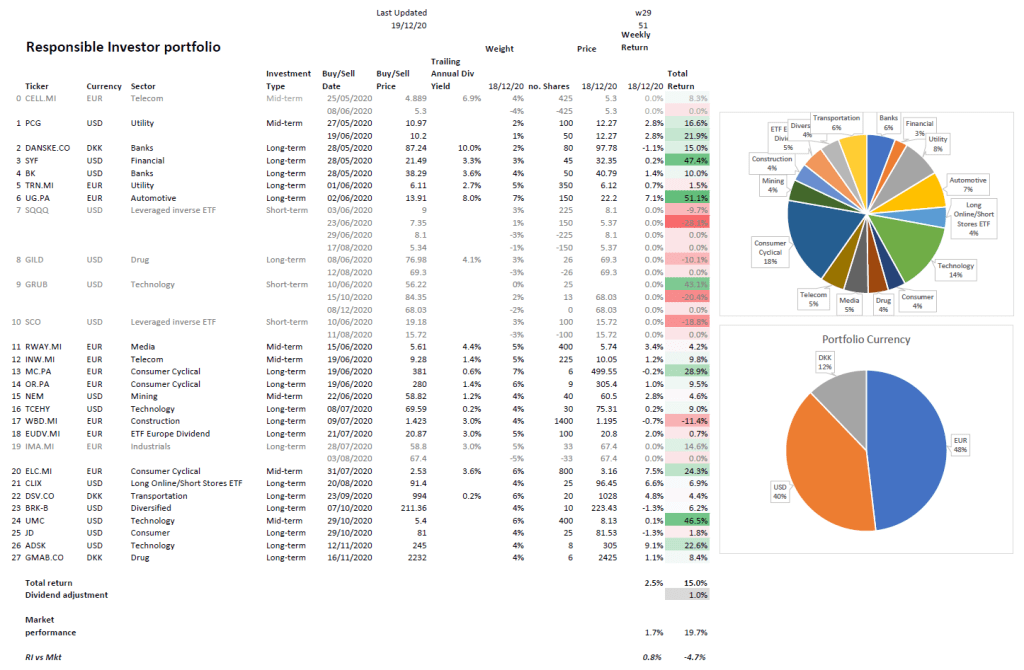

We beat the market this week, as our portfolio rose 2.5% versus a weighted average gain of the relevant market indices of 1.7% (+0.8% beat).

$UG.PA was up 7.1% this week and 51.1% overall. It now weighs 7% in our portfolio: I will be looking to scale down our position on pull backs as I don’t like to be too invested in a single stock. Other notable weekly jumps were observed in $ADSK (+9.1%) and $ELC.MI (+7.5%).

Our Responsible Investor portfolio is now up 15.0% (16.0% including dividends) in 29 weeks. We are about 56% in stocks & ETFs and 44% in cash. On my watchlist this week I have $DVA, $CMG, $COUP, $AMT, $AVGO and $ADBE.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.