Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “From credit crunch to credit crisis: brace for impact!”, and was written on March 25th, 2023.

Weekly summary in a paragraph

All the US stock market indices finished higher in a week which saw a 0.25% interest rate increase by the Fed and a dovish commentary. Consensus sees a 90% probability for a rate hike pause at the May FOMC meeting. The banking sector continued borrowing at a pace which reduced the systematic quantitative tightening by a third. Europe had a strong week despite concerns of the Credit Suisse contagion spreading to Deutsche Bank. 94% of European Stoxx 600 companies have reported Q4 2022 earnings now, with an 8% growth which is superior compared to the US (-5%). The 10-y yield continued its fall and resulted in the 2-10y spread dropping again this week to reach -38 basis points. Recall that the spread had reached -107 basis points just two weeks ago. In corporate news, Activision sees the concerns of its merger with Microsoft alleviated, and Disney announced the layoff of 7000 staff at its ESPN unit.

Asset classes weekly performance

This week the Dow finished +1.18% higher (-2.7% year to date) while the S&P500 gained +1.39% (+3.4% year to date), the Nasdaq rose +1.66% (+13.0% year to date) and the Russell 2000 appreciated +0.52% (-1.49% year to date, we have a 3x short position). Gold finished +2.06% higher (+6.39% year to date, we are long) while Silver gained +4.19% (-4.27% year to date). Oil was -0.67% weaker (-10.51% year to date). The 10-y US treasury yield tanked -6.27% (-10.89% year to date). The European stock market gained +2,89% (+10.5% year to date). The Euro finished +0.79% lower against the US Dollar (+0.5% year to date).

Weekly pitch

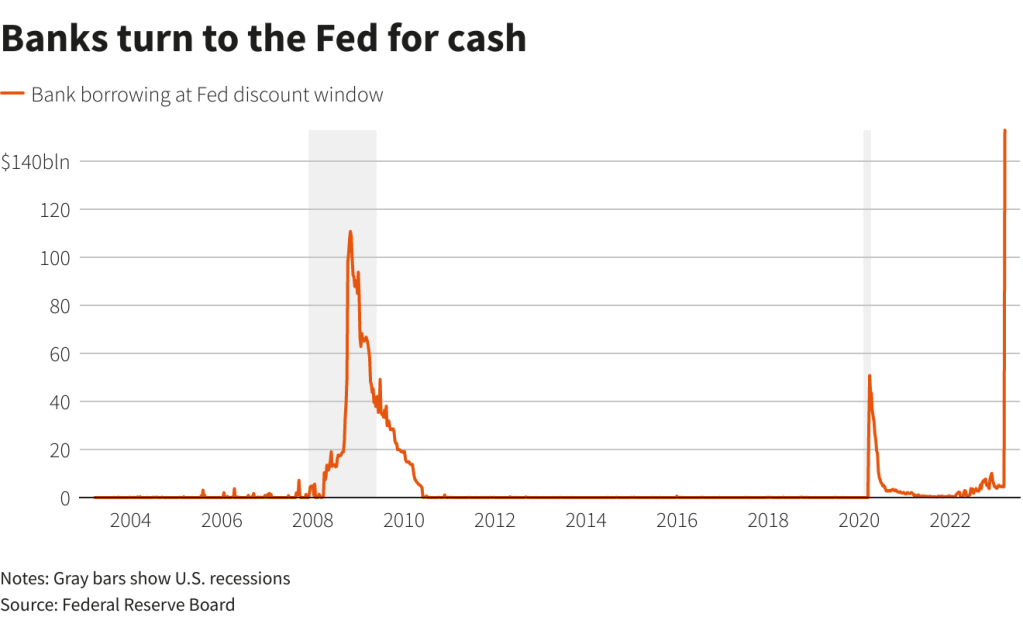

If you have been affected by the great financial crisis of 2007-2008, you will remember the challenge of borrowing money over that period: whether it is retail or commercial loans, this is what happens in a credit crunch. A credit crisis, however, is a much serious economic phenomenon whereby the banks themselves struggle to borrow either from each other or from the central banks. The graph below shows that the amount banks have borrowed at the Fed discount window in 2023 has exceeded the 110 billion USD top from the GFC and is near-vertical. The earnings decline and the credit crisis are two reasons to stay nimble if you are invested in the stock market. In order to protect yourself on the downside, responsible investors should raise cash, buy hedges (including precious metals and carefully selected corporate bonds) and be well-diversified.

Weekly Portfolio Update

Here are this week’s movements: we took profits on our Newmont Mining (+8.1%) and ACI Worldwide (+6.3%) long positions; we initiated new long positions on Halliburton, EOG Resources and MP Materials. Sell stops were triggered on our Adobe and Lennar shorts and on our US Banks ETF. Cash, precious metals and hedges amount to 39.5% in our portfolio (reduced compared to last week).

Top 5 Weekly Portfolio Performers

Sanofi +8.44% (Pharmaceuticals)

Sonoco Products +7.95% (Process Industries)

Meta +5.32% (Technology)

Electronic Arts +5.01% (Gaming)

Denbury Resources +4.63% (Oil)

Portfolio Asset Allocation

US Long stock positions 51.5% (increased)

EU Long stock positions 9% (unchanged)

US Short stock position 3% (reduced)

Hedges 7.5% (increased)

Silver & Gold 5% (unchanged)

Cash 24% (increased)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is -4.4% (excl. dividends) vs the S&P500 loss of -12.2%, which corresponds to a +7.8% market beat.

Invest responsibly!!!