Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Which key word did Fed Chair Powell not utter?”, and was written on May 6th, 2023.

Weekly summary in a paragraph

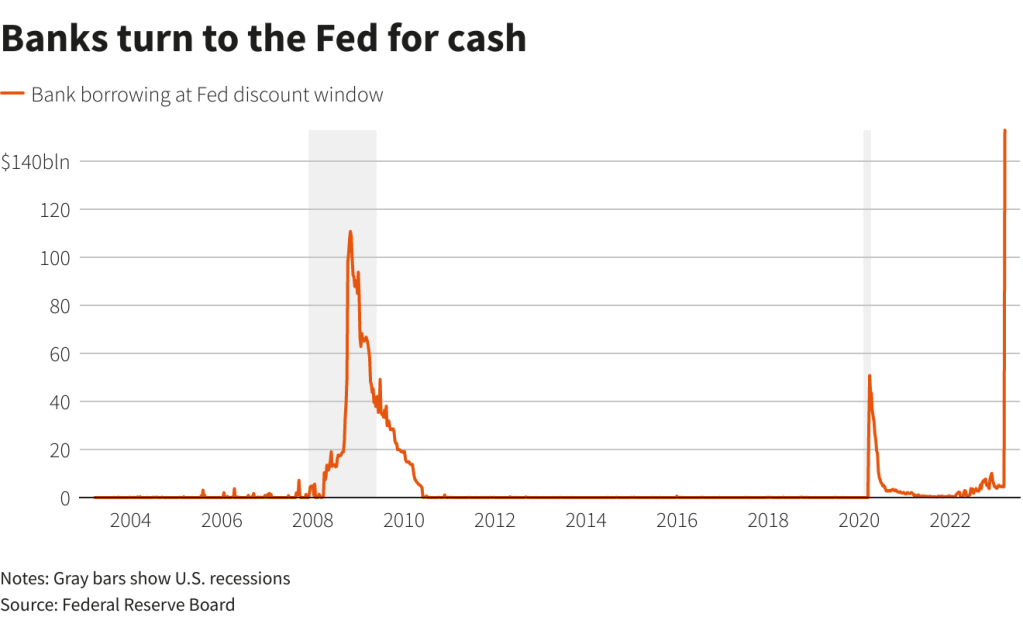

The US stock market indices finished mostly lower this week, with the exception of the Nasdaq which managed to gain a meager 0.1%. The week was dominated by the FOMC meeting which confirmed the 0.25% increase in interest rate, as expected. There was one key word which the Fed’s chair Powell did not utter, though: “pause”. In other words, the Fed will keep making decisions on the basis of economic data, and is not prepared to commit to this latest increase being the last in the cycle. The European stock market finished higher and is still leading year to date, globally, despite this week’s ECB rate hike. The 2-10y spread reversed its trend and reduced the gap to an inverted value of -48 basis points. In terms of economic data, the ISM index published on Monday was slightly better than consensus, and the jobs report came in stronger than expected on Friday. In corporate news, Apple beat earnings and saved the market from an even deeper weekly loss, though this is the second quarter in a row that Apple revenue has decreased. Next week more S&P500 companies report earnings, including Paypal, Airbnb and Disney.

Asset classes weekly performance

This week the Dow finished -1.24% lower (+1.6% year to date) while the S&P500 gave up -0.8% (+7.7% year to date), the Nasdaq advanced +0.1% (+16.9% year to date) and the Russell 2000 lost -0.5% (-0.1% year to date). Gold finished +0.1% higher (+7.8% year to date, we are long) while Silver gained +1.21% (+5.4% year to date, we are long). Oil lost -0.5% (-7.7% year to date). The 10-y US treasury yield gave up -0.2% (-9.2% year to date). The European stock market gained +0.2% (+19.9% year to date). The Euro appreciated +0.11% against the US Dollar (+2.92% year to date).

Weekly pitch

Strong economic data and the Fed’s refusal to pivot were responsible for a negative week. While the quarter percentage point rate hike was largely expected, the market was looking for the Fed to confirm that no further hikes were planned, and were therefore disappointed by Powell’s words during the press conference. Despite the proximity of the war in Ukraine, the performance of the European stock market and of the Euro keeps being superior relative to the US indices and the US dollar. Responsible investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market. This week we have beaten the market, taken full profits on long positions and initiated new long positions.

Weekly Portfolio Update

Here are this week’s movements: we took profits on our Arconic Corporation (+17%), Electronic Arts (+10.6%) and Sanofi (+9.1%) long positions; sell stops were triggered on our Capri Holdings and on the US Banks ETF long positions. We initiated long positions on Plug, Restaurants Brands International and AMD. Cash, precious metals and hedges amount to 41% in our portfolio (increased compared to last week).

Top 5 Weekly Portfolio Performers

Arconic Corporation +17.4% (Aluminum)

Rational +7.8% (Industrial Machinery)

Sibanye Stillwater +7.4% (Precious Metals)

Davide Campari +4.6% (Alcoholic Beverages)

Marriot International +4.3% (Hotels & Leisure)

Portfolio Asset Allocation

US Long stock positions 49.5% (reduced)

EU Long stock positions 9.5% (reduced)

US Short stock position 4.5% (increased)

Hedges 8% (increased)

Silver & Gold 3.5% (unchanged)

Cash 25% (unchanged)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is +5.2% (excl. dividends) vs the S&P500 loss of -0.3%, which corresponds to a +5.5% market beat.

Invest responsibly!!!