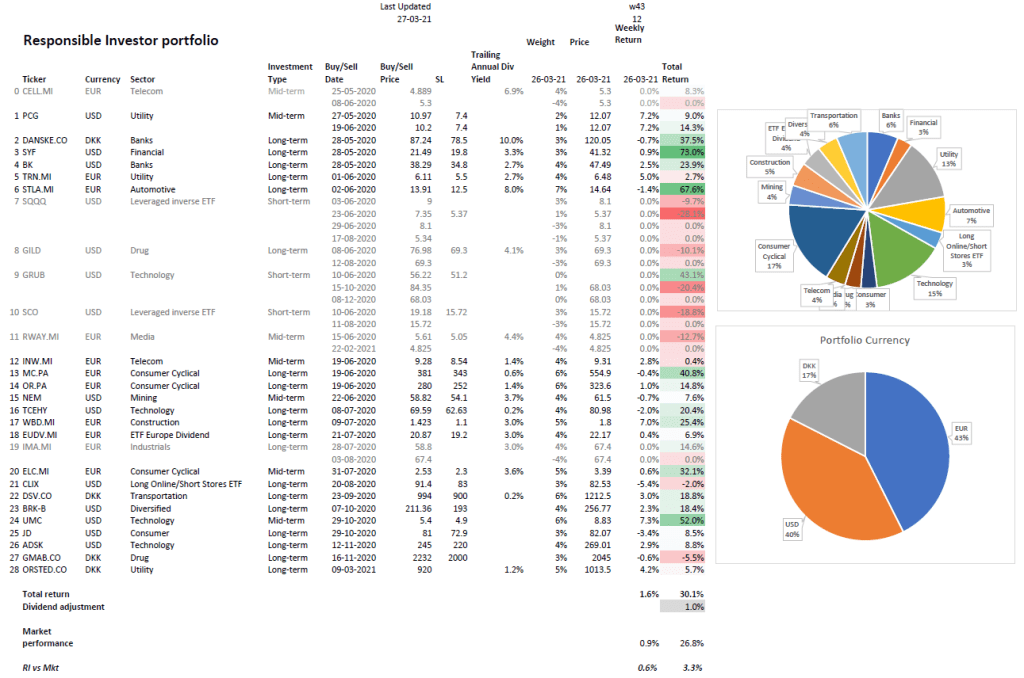

Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Earnings surprise! What to do now”, and was written on April 29th, 2023.

Weekly summary in a paragraph

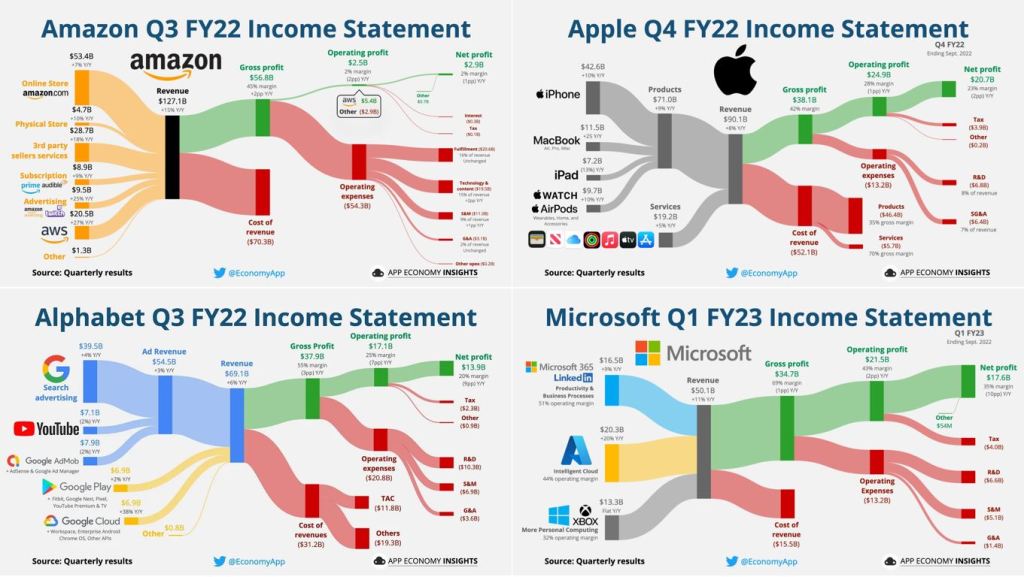

The US stock market indices finished higher this week, though the Russell 2000 didn’t participate. Q1 GDP data published this week reported a 1.1% growth in the US while the Europe area stopped at 0.1%, and avoided a recession by a hair. The European stock market saw an end to multi-week gains but is still leading year to date, globally. The 2-10y spread was flat and is still inverted at -60 basis points. Oil now in negative territory after the first four months of 2023. In terms of economic data, March headline and core PCE inflation came in mostly in line. Personal income and spending for March was reported slightly higher than expected. In corporate news, mega cap companies like Microsoft and Meta smashed Q1 2023 earnings, Alphabet reported a beat while Amazon’s guidance underwhelmed. Many other long positions in our portfolio reported an earnings beat this week, Chipotle and Fielmann above all. Next week 126 S&P500 companies report earnings, including AMD, Apple and Novo Nordisk.

Asset classes weekly performance

This week the Dow finished +0.86% higher (+2.9% year to date) while the S&P500 gained +0.87% (+8.6% year to date), the Nasdaq advanced +1.28% (+16.8% year to date) and the Russell 2000 lost -1.26% (+0.4% year to date). Gold finished flat (+6.5% year to date, we are long) while Silver lost -0.74% (+3.0% year to date, we are long). Oil tanked -2.7% (-0.8% year to date). The 10-y US treasury yield gave up -1.79% (-9.0% year to date). The European stock market lost -0.4% (+19.7% year to date). The Euro gained +0.24% against the US Dollar (+2.9% year to date).

Weekly pitch

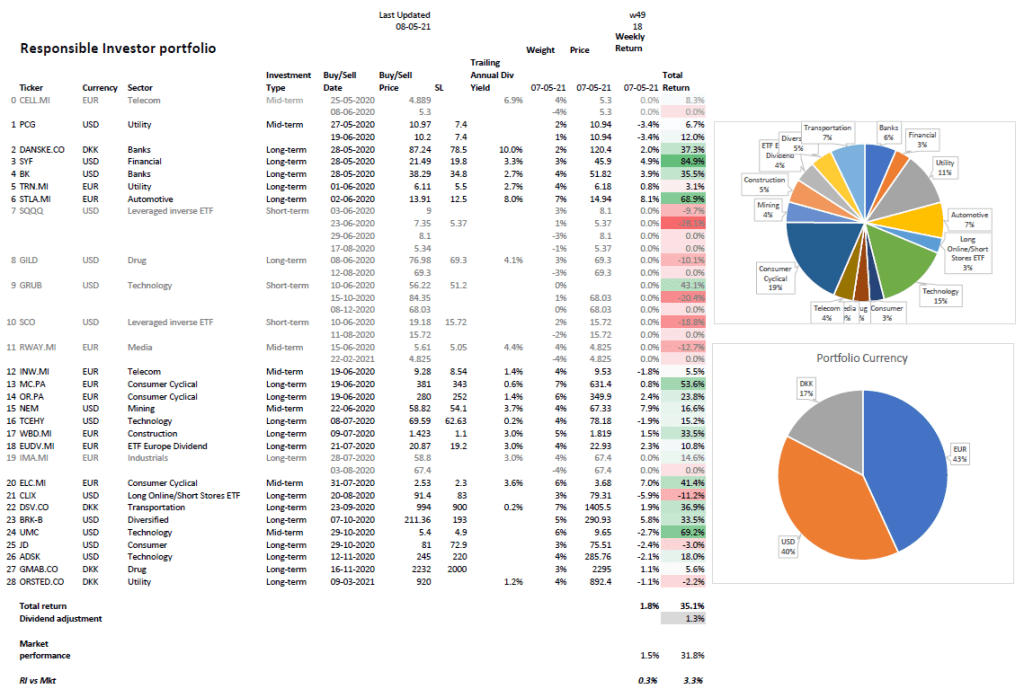

The earnings estimate for the S&P500 companies in Q1 2023 was just over 50$, in aggregate, at the beginning of the earnings season. After 222 companies reported so far that number has increased by 2.5%. If this increase is representative of the other half which will report in May, the overall figure may increase to 54-55$, ie one of the largest in recent years. It is important to note, however, that the year to date increase on the index is led by very few companies, therefore now more than ever before it is a stock picker’s market. Until more earnings data is available over the next couple of weeks, responsible investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges. Analysts now believe that another quarter point rate hike will happen at next week’s FOMC meeting, with an 86% probability. This week we have taken full or partial profits on long and short positions and initiated new long positions.

Weekly Portfolio Update

Here are this week’s movements: we took profits on our Eli Lilly (+13.9%) long position, on our Snapchat (+2.6%) and Pinterest (+16%) short positions and partial profits on our Microsoft (+15.3%), Halliburton (+4.5%), Raytheon Technologies (+4.3%), Sibanye Stillwater (+4.2%) and Capri Holdings (+3.6%) long positions. We initiated long positions on three Chinese ETFs. Cash, precious metals and hedges amount to 40% in our portfolio (increased compared to last week).

Top 5 Weekly Portfolio Performers

Fielmann +16.43% (Medical Specialties)

Chipotle Mexican Grill +14.87% (Restaurants)

Meta +12.88% (Technology Services)

Microsoft +7.52% (Technology Services)

Centene +4.46% (Managed Healthcare)

Portfolio Asset Allocation

US Long stock positions 50% (reduced)

EU Long stock positions 10% (unchanged)

US Short stock position 4% (reduced)

Hedges 7.5% (unchanged)

Silver & Gold 3.5% (reduced)

Cash 25% (increased)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is +4.2% (excl. dividends) vs the S&P500 loss of -2.8%, which corresponds to a +7.0% market beat.

Invest responsibly!!!