$WSM $VWS.CO $CALM $NVDA $GIS $SRTY $KBE $CSCO $DEN $LIT $QCOM $BRK.B $SIG $NUE $PLUG $TELL $DIS $THO $MP $KSS $GL $WMT $TGT $GILD $AIG $ORI $USB $CNC $SH $GLD $SLV $SON $NEM $HLT $NXPI $DEN $GPS $JPM $CMG $MSFT $META $BWA $LEA

Weekly summary in a paragraph

While the Santa rally did not materialise, the first trading week of 2023 did not disappoint for stock markets around the world which finished higher. In the US the 4 days of trading were choppy with the Friday session bringing it home thanks to the justification which came from falling ISM services and a less than expected rise in the average hourly earnings, both of which offset the strong jobs report.

The stock market rally continued in China, particularly for tech, as investors are bullish on rumours that the crack-down on publicly listed companies may ease. Europe outperformed the US even though its gains were offset by a sharp weakening of the Euro relative to the Dollar.

There is a growing bullish sentiment, even in the Nasdaq who some analysts believe to have found the bottom. With the Q4 earnings season due to kick off next week, investors need to remain vigilant as this will be a key quarter to watch for signs of weakness especially with regards to 2024 estimates: the markets are forward-looking!

Asset classes weekly performance

This week the Dow gained +1.45% (+1.45% YTD) just like the S&P500 (+1.45% YTD, we are 1x short), the Nasdaq finished +0.98% higher (+0.98% YTD, we have a 3x inverse position) and the Russell 2000 gapped up +2.4% (+2.4% YTD, we are 1x short). $Gold finished higher +2.4% (2.4% YTD) while silver was -0.6% lower (-0.6% YTD). $Oil fell sharply by -4.1% (-4.1% YTD). The 20-y was markedly higher with a +3.7% gain this week (+3.7% YTD). The European stock market gained +4.7% (+4.7% YTD). The Euro gave up -1.5% against the USD (-1.5% YTD).

Weekly pitch

5 things I got right in 2022:

- Sold $AAPL and $GOOG close to the peak (August), plus other long-duration stocks which do not do well in a rising interest rate environment

- Hedged, including raising cash

- Sold short $TLT

- Monitored the markets more closely than I would do in a bull market

- Followed macro trends and invested accordingly, for example in oil and energy stocks in general

..and 5 I got wrong:

- Did not hedge enough and early enough

- Did not exploit the energy rally enough and missed the opportunity to invest in LNG stocks

- Was too attached to some of my historical long positions without sufficient justification

- Covered the $TLT short too early in the year

- Partly missed the rally in commodities

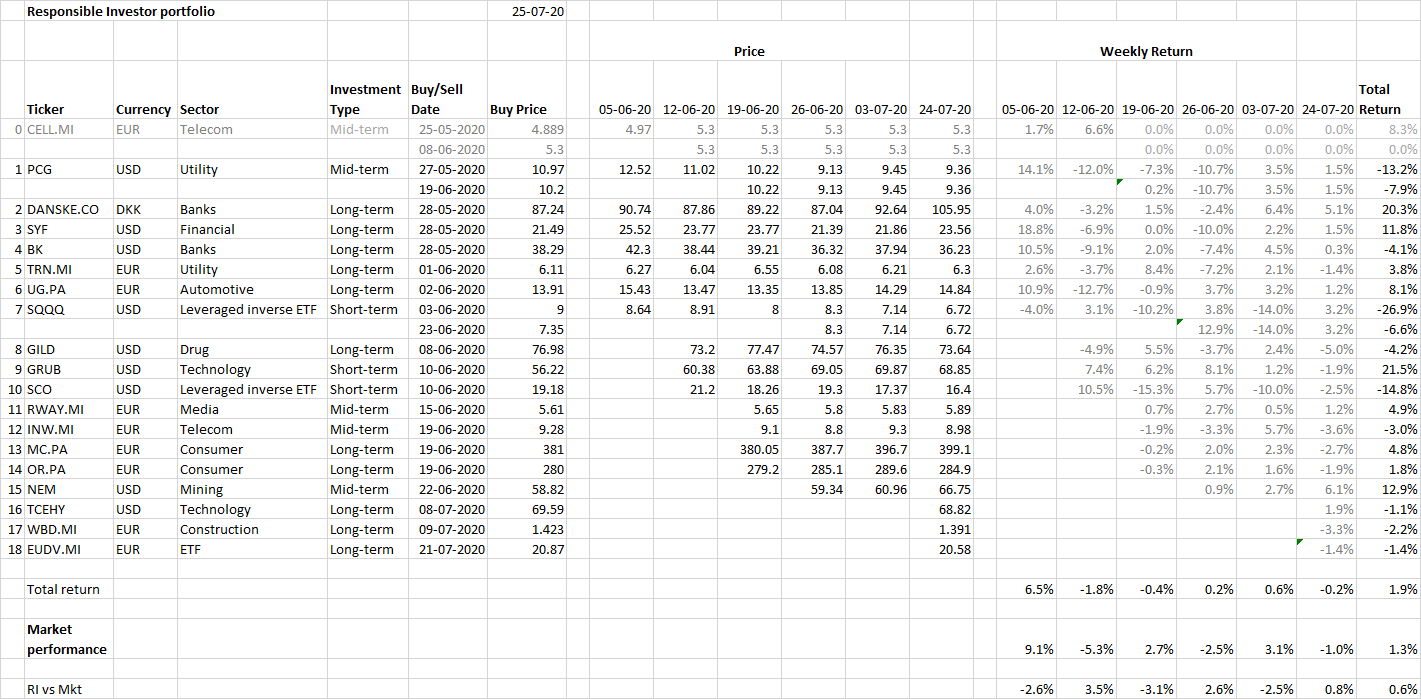

Weekly Portfolio Update

Here are this week’s movements: we started a position in the Danish company $VWS.CO, we accumulated on our long position in $META, took profits on the $CSCO short position and initiated a sells position on $WSM. Cash, precious metals, hedges and short stock positions amount to 41% in our portfolio (reduced compared to last week).

Top 5 Weekly Portfolio Performers

$NEM +11.53% (Precious metals)

$FCX +11.26% (Precious metals)

$MC.PA +10.44% (Luxury)

$THO +10.24% (Consumer durables, recreational products)

$SBSW +9.38% (Precious metals)

Portfolio Asset Allocation

Long stock positions 59% (increased)

Short stock position 4% (increased)

Hedges 9% (unchanged)

Silver & Gold 4% (unchanged)

Cash 24% (reduced)

YTD Portfolio Performance

Our currency-adjusted YTD portfolio performance in Euro is +0.22% (excl. dividends) vs the European market gain of +3.2% and the S&P500 gain of 1.45% (+0.27% US market beat, expressed in $).

Invest responsibly!!!