Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Oil production cut and the spectre of stagflation”, and was written on April 8th, 2023.

Weekly summary in a paragraph

The US stock market indices were mixed in a 4-day week of trading which was dominated by the surprise oil production cut by OPEC (more in the weekly pitch). Economic data included the ISM manufacturing PMI on Monday and non-manufacturing PMI on Wednesday which both missed, and the March nonfarm payroll data which came in near expectations on Friday. The European stock market continued to show its strength and so did the Euro. The 2-10y spread finished flat at -52 basis points. In corporate news, Fedex announced a restructuring and General Motors overtook Toyota as the top US automaker last year. Next week the Q1 2023 earnings season kicks off: any significant misses may result in another market leg down.

Asset classes weekly performance

This week the Dow finished +0.7% higher (+1.02% year to date) while the S&P500 lost -0.1% (+6.9% year to date), the Nasdaq gave up -1.1% (+15.5% year to date) and the Russell 2000 tanked -2.5% (-0.39% year to date, we have a 3x inverse position). Gold finished +1.8% higher (+7.8% year to date, we are long) while Silver gained +3.4% (+3.0% year to date, we are long). Oil was +6.5% higher (+4.05% year to date). The 10-y US treasury yield lost -6.1% (-13.3% year to date). The European stock market gained +0.7% (+16.8% year to date). The Euro finished +0.7% higher against the US Dollar (+1.84% year to date).

Weekly pitch

Rumour has it that OPEC decided to cut oil production by 1.6 million barrels as a reaction to Biden’s decision to not refill the Strategic Petroleum Reserve (SPR). For us investors the main consequence is that this is an inflationary move which comes at a rather delicate time: will it delay the Fed’s pivot? The main reason inflation has cooled off lately is that energy prices have come down from the 2022 cycle highs: if oil prices go up, the risk of stagflation will increase and this may contract earnings. Last week we went over the strong link that exists between earnings and stock prices, hence prudence is of the essence. In order to protect themselves on the downside, responsible investors should raise cash, buy hedges (including precious metals and carefully selected corporate bonds) and be well-diversified.

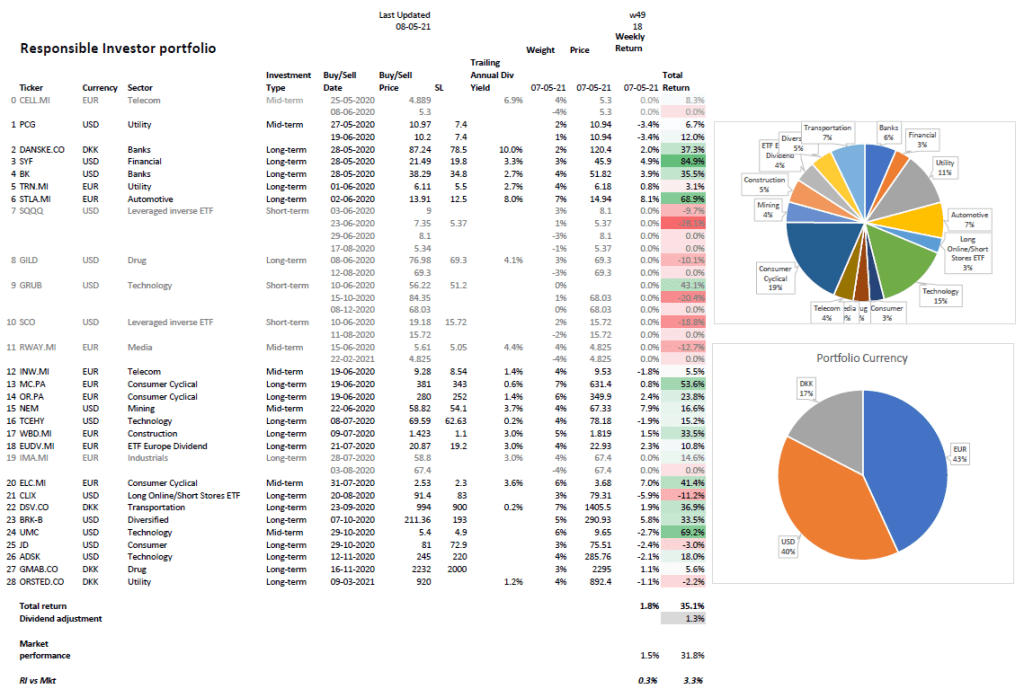

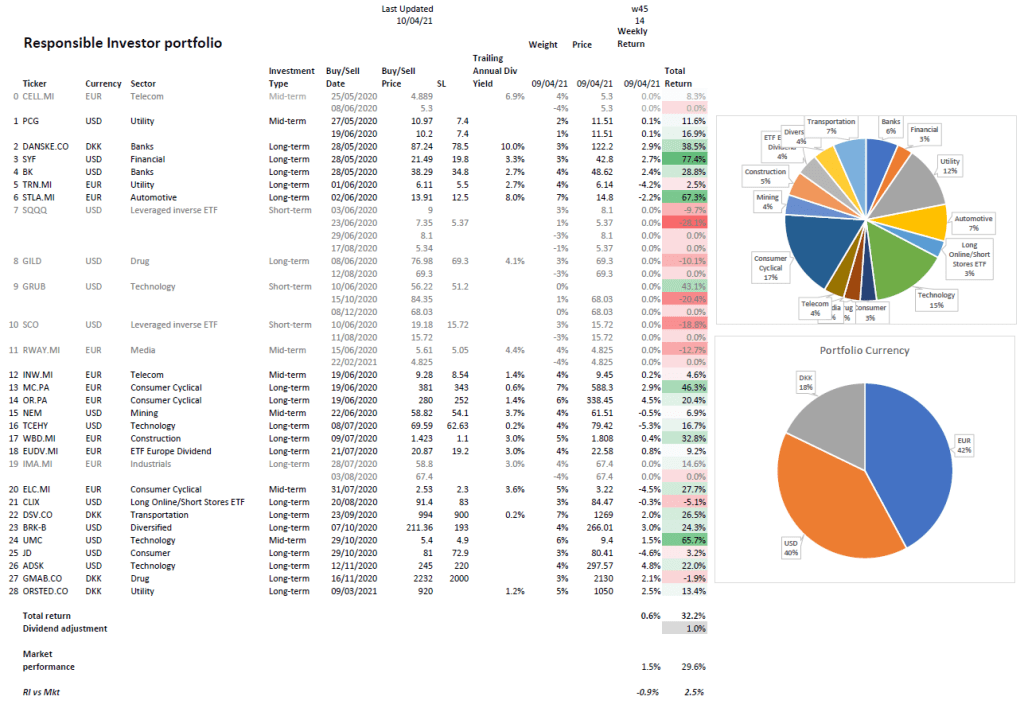

Weekly Portfolio Update

Here are this week’s movements: we took profit on our World Wrestling Entertainment long position (+3.0%). Cash, precious metals and hedges amount to 39.5% in our portfolio (unchanged compared to last week).

Top 5 Weekly Portfolio Performers

Ely Lilly & Co. +7.24% (Pharmaceuticals)

ProShares UltraPro Short Russell 2000 +8.11% (3x short the Russell 2000)

Newmont Mining +6.18% (Precious metals mining)

Denbury Resources +5.84% (Oil)

Callon Petroleum +5.80% (Oil)

Portfolio Asset Allocation

US Long stock positions 51.5% (unchanged)

EU Long stock positions 9% (unchanged)

US Short stock position 4% (increased)

Hedges 7.5% (unchanged)

Silver & Gold 5% (unchanged)

Cash 23% (reduced)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is -1.5% (excl. dividends) vs the S&P500 loss of -8.8%, which corresponds to a +7.3% market beat.

Invest responsibly!!!