Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Did the ECB send a bullish signal to the stock market?”, and was written on September 16th, 2023.

Weekly summary in a paragraph

The US stock market indices finished mostly lower this week, except the Dow which rose marginally in a week which was affected by a significant sell-off on Friday despite the success of the ARM IPO. The European stock market ended its 6-week negative streak and returned to gains despite the euro continued weakness relative to the dollar. The ECB hiked interest rates by another 0.25%. The 2-10y spread tightened slightly this week and is still inverted at -69 basis points. In economic data, the core inflation (CPI) as well as the inflation at producer level (PPI) are running hotter than expected. Retails sales data were also strong which indicates further borrowing by the consumer. In corporate news, both Adobe and Lennar dipped despite beating Q2 earnings expectations. The launch of the new Apple models and the French ban on the iPhone 12 did not help the stock which fell this week. Despite the vast majority of the S&P500 companies having now reported Q2 earnings, there are still notable ones due to be published next week such as Stitch Fix, Autozone, General Mills, Fedex and Kb Home.

Asset classes weekly performance

This week the Dow finished +0.1% higher (+4.4% year to date) while the S&P500 lost -0.2% (+15.9% year to date), the Nasdaq gave up -0.4% (+31.0% year to date) and the Russell 2000 fell -0.2% (+4.9% year to date). Gold finished -0.1% lower (+1.0% year to date) while Silver lost -0.3% (-7.2% year to date). Crude Oil gained +4.5% (+20.3% year to date). The 10-y US treasury yield rose +0.8% (+14.0% year to date). The European stock market gained +0.8% (+12.9% year to date). The Euro lost -0.52% against the US Dollar (-0.45% year to date).

Weekly pitch

One of the ways central banks fight inflation is through increasing interest rates. Both the Fed and the ECB have been using this weapon over the past months. Following this week’s inflation data, there is now a 40% chance that the Fed will hike again in November. The ECB just hiked interest rates this week though the significant news is that it suggested it may be done for this cycle. This is a bullish signal for the stock market and also for the bonds of the EU member states. Responsible Investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market and to emerging markets.

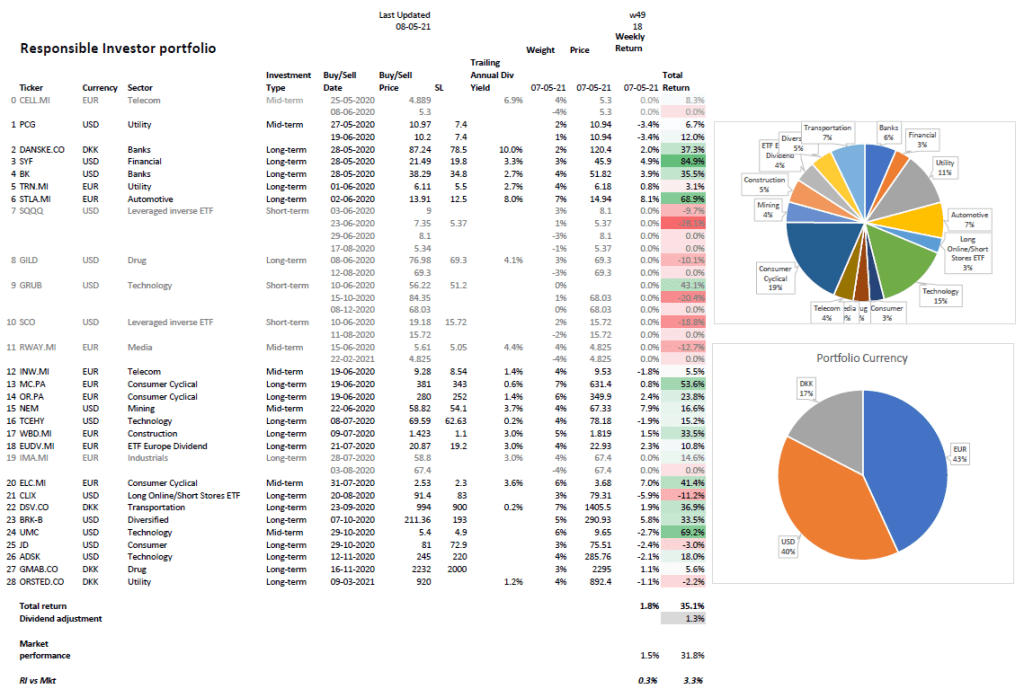

Weekly Portfolio Update

No movements this week. Cash, US treasury bills, precious metals and hedges amount to 38.5% in our portfolio (unchanged compared to last week). It was a good week for our precious metals stocks.

Top 5 Weekly Portfolio Performers

Sibanye Stillwater +16.7% (Precious metals)

ProShares UltraPro Short QQQ +5.3% (3x inverse the Nasdaq)

MP Materials +4.4% (Rare-earth materials)

Newmont Mining +3.6% (Precious metals)

Denbury Resources +3.3% (Oil)

Portfolio Asset Allocation

US stocks long positions 44.5% (unchanged)

EU stocks long positions 8.5% (unchanged)

Emerging markets long positions 4.5% (unchanged)

US stocks short positions 4.0% (unchanged)

Hedges 8.0% (unchanged)

Silver & Gold 2% (unchanged)

US Treasury bills 2% (unchanged)

Cash 26.5% (unchanged)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is +11.8% (excl. dividends) vs the S&P500 gain of +14.1%.

Invest responsibly!!!