Gold experienced extraordinary volatility, with a massive $5.5 trillion swing highlighting how fragile positioning has become. Early in the session, retail momentum traders piled aggressively into gold and silver vehicles, exhausting buying power just before a sharp drop. Once selling pressure peaked, dip buyers stepped in, reinforcing how crowded and reactive the trade has become. Silver was even more extreme, trading through a staggering 24.5% intraday range, underscoring the speculative intensity across precious metals.

Market dynamics shifted further as speculation emerged that President Trump would nominate Kevin Warsh as the next Federal Reserve Chair. Selling pressure in gold accelerated on the rumor and continued after the nomination was confirmed. The reaction reflects uncertainty around future monetary policy rather than a simple hawkish or dovish interpretation. While Warsh is viewed historically as hawkish, his credibility may give him greater influence within the FOMC, where policy outcomes depend on consensus rather than the chair alone.

Inflation data added to the tension. Producer prices surprised to the upside, with both headline and core readings coming in hotter than expected, reinforcing concerns that inflation pressures remain sticky. Taken together, volatile commodities, shifting Fed expectations, and firm inflation data suggest markets remain highly sensitive to policy signals. Investors are closely watching $GLD, $SLV, $GDX, $SPY, and $TLT as these crosscurrents continue to drive sharp moves.

Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Is the market more worried about inflation or recession?”, and was written on July 8th, 2023.

Weekly summary in a paragraph

The US stock market indices finished lower this week, with all the major indices giving up most of last week’s gains. Volume was lower as the summer season kicked off with Independence Day.

The European stock market underperformed the US stock market though the Euro appreciated relative to the US Dollar.

The 2-10y spread reduced after weeks of widening but is still inverted at -88 basis points.

Economic data this week included a weaker than expected jobs report which fuelled a rebound in stocks on Friday.

In corporate news, Meta’s new Threads, a competitor of Twitter, beat expectations in terms of initial subscribers while Samsung announced a concerning profit-warning.

Next week Q2 earnings kick off with some of the large US banks reporting, such as JP Morgan Chase, City and Wells Fargo. Delta and Unitedhealth are reporting also.

Asset classes weekly performance

This week the Dow finished -2.0% lower (+2.1% year to date) while the S&P500 lost -1.2% (+15.0% year to date), the Nasdaq gave up -0.9% (+31.3% year to date) and the Russell 2000 was -1.3% weaker (+7.8% year to date). Gold finished +0.2% higher (+4.7% year to date) while Silver gained +1.4% (-3.3% year to date). Oil jumped +4.4% (-4.0% year to date). The 10-y US treasury yield gained +5.8% higher (+6.0% year to date). The European stock market lost -2.8% (+18.8% year to date). The Euro gained +0.5% against the US Dollar (+2.9% year to date).

Weekly pitch

The stock market did not have much data to justify an up week which meant that down was the path of least resistance. This week two main events are expected to shape the market: the all-important CPI report on Wednesday and the first significant group of large US banks reporting their Q2 earning on Friday. Any match or exceedance of the CPI expectation is likely to send the market higher in the short term. Q2 earnings and earnings forecasts for 2024 will govern long term market moves.Until the current Q2 earnings expectations are confirmed, responsible investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market.

Weekly Portfolio Update

Here are this week’s movements: we took profits on our Dish Network (+10%) and our MP long position (+5.2%). We have also initiated a 2% long position on 1 to 3 year US Bonds which seem attractive at near-peak interest rates. Cash, US treasury bills, precious metals and hedges amount to 43% in our portfolio (increased compared to last week).

Top 5 Weekly Portfolio Performers

Tellurian +17.4% (Energy Minerals)

Halliburton +14.9% (Oilfield Services)

DraftKings +14.9% (Entertainment)

Range Resources +6.7% (Oil)

Marriott International +6.4% (Hotels)

Portfolio Asset Allocation

US stocks long positions 48.5% (reduced)

EU stocks long positions 8.5% (unchanged)

US stocks short position 3% (increased)

Hedges 8.0% (unchanged)

Silver & Gold 2% (unchanged)

US Treasure bills 2% (initiated)

Cash 28% (reduced)

1-year Portfolio Performance

Our portfolio performanceover the last 12 months is +12.9% (excl. dividends) vs the S&P500 gain of +12.7%, which corresponds to a 0.2% market beat.

Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “What is ‘window dressing’ and why does it matter?”, and was written on July 1st, 2023.

Weekly summary in a paragraph

The US stock market indices finished higher this week, with all the major indices recovering after last week’s decline. The Nasdaq has had the best first half of the year ever. The European stock market outperformed the US stock market as the Eurozone flash PMI came in lower than expected, and is ahead of the S&P500 for the third quarter in a row. The 2-10y spread continues to widen and has now an inverted value of -106 basis points. Economic data published this week was mostly positive. In speaking at an event in Europe, Powell stated that future hikes are still a possibility. In corporate news, Carnival beat expectations while Nike and Micron missed. No major earnings reports next week. The Q2 earnings seasons kicks off week after next with some of the largest US banks reporting on Friday the 14th of July.

Asset classes weekly performance

This week the Dow finished +2.02% higher (+3.8% year to date) while the S&P500 gained +2.35% (+15.9% year to date), the Nasdaq soared +2.19% (+31.7% year to date) and the Russell 2000 jumped +3.68% (+7.2% year to date). Gold finished +0.2% higher (+1.8% year to date) while Silver gave up -0.7% (-7.4% year to date). Oil gained +4.1% (-8.1% year to date). The 10-y US treasury yield was +1.35% higher (+0.69% year to date). The European stock market gained+3.6% (+18.8% year to date). The Euro lost -0.1% against the US Dollar (+1.8% year to date).

Weekly pitch

There wasn’t enough in the economic data reports to sustain the rally that all major indices experienced this week. The end of Q2, however, meant that fund managers were busy with the so-called ‘window dressing‘, an investment practice whereby money managers sell laggards in their portfolio and buy stocks which have had a good run. That way, their portfolios appear to be full of winners. Fund managers move a lot of money in the markets and window dressing may have masked what would have otherwise been a quiet week. Until the current Q2 earnings expectations are confirmed, responsible investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market.

Weekly Portfolio Update

Here are this week’s movements: we took partial profits on our Campari long position (+22%), as well as full profits on our ASX long position (+6.5%) and our UPS short position (+4.4%); a stop loss was triggered on our Thor short position. Cash, precious metals and hedges amount to 42% in our portfolio (increased compared to last week).

Top 5 Weekly Portfolio Performers

Callon Petroleum +9.6% (Oil)

Dish Network +9.5% (Cable/Satellite TV)

BorgWarner +8.1% (Trucks)

Marriott +7.1% (Hotels)

ACI Worldwide +7.0% (Tech)

Portfolio Asset Allocation

US stocks long positions 49.5% (unchanged)

EU stocks long positions 8.5% (reduced)

US stocks short position 2% (unchanged)

Hedges 8.0% (unchanged)

Silver & Gold 2% (unchanged)

Cash 30% (increased)

1-year Portfolio Performance

Our portfolio performanceover the last 12 months is +14.0% (excl. dividends) vs the S&P500 gain of +16.5%.

A mildly positive inflation data point on Wednesday was all it took to send the global stock markets higher and induce weakness in the US dollar. I don’t want to be the Cassandra of the situation here, but one month on month data point does not seem enough to justify a reversal of the general trend though technical analysis would suggest further strength ahead at least in the short term.

It was an even stronger week for the European stock market which was further amplified by strength in the Euro.

Asset classes weekly performance

This week the Dow gained +4.1% (-7.2% YTD) while the S&P500 went +5.6% higher (-16.2% YTD, we are 1x short), the Nasdaq skyrocketed +8.0% (-29.0% YTD, we have a 3x inverse position) and the Russell 2000 gained +4.6% (-16.7% YTD, we are 1x short). $Gold rose +5.2% (-4.4% YTD) while silver finished +3.6% higher (-7.2% YTD). $Oil gave up -4.0% (+18.3% YTD). The 20-y recovered +3.9% this week (-33.7% YTD). The European stock market outperformed the US market indices and finished +9.6% higher (-19.2% YTD). The Euro recovered as much as +4.0% relative to the USD (-11.5% YTD).

Weekly pitch

As most of the S&P500 companies have reported Q3 earnings, there is now sufficient data to update earnings forecasts. This week Goldman Sachs revised their S&P500 earnings forecast to the downside ($224 USD) to conclude that they now expect zero earnings growth for 2023. Because stocks follow earnings and earnings expectations, investors will now have to look to 2024 (current estimate is $237 hence +6% compared to ’22 and ‘23) to justify staying invested on the long side.

Weekly Portfolio Update

We initiated three new positions on $NEM, $KSS, and $USB which are already profitable trades. We have also increased our position in gold: if dollar continues its weakness this will send its price higher. Cash, precious metals and hedges were reduced to 37% in our portfolio which rose +2.77% this week.

Top 5 Weekly Portfolio Performers

$META +24.49% (Technology-Social Media)

$FTNT +19.17% (Technology-Software-Security)

$THO +17.38% (Building-Mobile Manufacturing/RV)

$DUE.DE +15.52% (Industrial – Germany)

$KSS +15.24% (Consumer-Dept. Stores)

Portfolio Asset Allocation

– Long stock positions 63% (increased)

– Hedges 9%, though equal to 14% considering leveraged ETFs (unchanged)

– Silver + Gold 4% (increased)

– Cash 24% (decreased)

YTD Portfolio Performance

Our currency-adjusted YTD portfolio performance is -2.2% (excl. dividends) vs the European market loss of -7.7% (+5.5% market beat).

A slew of positive economic data and a consistently hawkish Fed sent the US stock market lower this week. Despite indications that the next Fed’s interest rate hike may be contained to 0.5% after this week’s 0.75% increase, the jobs market is still too strong and inflation does not seem to slow down enough for the Fed to change its course such that the tightening monetary policy is limiting any upside potential at least in the short term.

On the other side of the pond, the European stock market staged the second week of gains.

Asset classes weekly performance

This week the Dow lost -1.4% (-11.9% YTD) while the S&P500 gave up -3.3% of gains (-20.9% YTD, we are 1x short), the Nasdaq tanked -5.6% (-33.9% YTD, we have a 3x inverse position) and the Russell 2000 lost -2.4% (-20.9% YTD, we are 1x short). $Gold gained +2.2% (-11.2% YTD) while silver skyrocketed +8.5% (-16.6% YTD). $Oil rose 4.9%. The 20-y recovered +5.7% this week (-35.3% YTD). The European stock market rose +1.3% (-28.3% YTD). The Euro finished flat against the USD (-13.3% YTD).

Weekly pitch

Following the marginal win of former president Lula, Brazil presents itself as more attractive economy to foreign investors. Additionally, rising oil prices are lifting the stock market since the Bovespa is heavily weighted on oil stocks such as $PBR which counts as 10% while the mining company $VALE reaches 15%. Former president Bolsonaro has not yet conceded though has signalled that he will collaborate in the transition. Brazil currently looks like an interesting investing opportunity unlike most of the emerging markets.

Weekly Portfolio Update

We initiated a position on the Brazilian stock market $EWZ which is already a profitable trade. We also went long on $USB, a regional US bank. We sold our positions on $PCTY and $FIS. Cash, precious metals and hedges were increased to 38% in our portfolio which beat the market by +2.2% this week.

Here are the top 5 performers of our portfolio this week:

$SQQQ +18.67% (3x inverse Nasdaq ETF)

$FCX +9.29% (Basic Materials-Metal Ores)

$SLV +8.57% (Silver ETF)

$EWZ +7.69% (Brazil Stock Market ETF)

$CPE +5.08% (Energy)

This is our asset allocation as things stand:

– Long stock positions 62% (increased)

– Hedges 9%, though equal to 14% considering leveraged ETFs (unchanged)

– Silver + Gold 3% (unchanged)

– Cash 26% (increased)

Our currency-adjusted YTD portfolio performance is -2.3% (excl. dividends) vs the European market loss of -15.0% (+12.7% market beat).

It was a tale of two stock markets in the US: while all the major indices continued to rally for the second week in a row, major tech companies reported poor earnings and most importantly week outlook which limited gains for the Nasdaq. Given the hotter than expected inflation data (core PCE came in at 0.5% vs 0.4% consensus) this recent optimism seems largely unjustified although we are heading towards a period of positive seasonality coupled with favourable technicals.

Asset classes weekly performance

This week the Dow gained +3.9% (-11.9% YTD) just like the S&P500 (-18.2% YTD, we are 1x short) and the Nasdaq limited its advance to +2.2% (-31.0% YTD, we have a 3x inverse position). The Russell 2000 skyrocketed +6.0% (-19.5% YTD, we are 1x short). $Gold lost 0.6% (-9.5% YTD) while silver finished flat -0.1% (-16.4% YTD). $Oil rose 3.4%. The 20-y recovered +5.7% this week (-34.2% YTD). The European stock market rose +4.9% (-26.5% YTD). The Euro recovered 1.0% against the USD (-10.9% YTD).

Weekly pitch

The four biggest tech companies in the US stock market all reported earnings this week. There are clear signs of weakness in all four although $AAPL appears more resilient. These are all companies full with an incredible pool of talented individuals though more short-term pain ahead is likely. We had exited our position in $AMZN and $AAPL at the beginning of August, just before they peaked. $META’s earnings were particularly concerning especially the reported losses from investments associated to the metaverse.

Weekly Portfolio Update

After the blowout earnings report $GILD rose sharply and finished with a 19% weekly gain: we have taken partial profit (+26.45%) on our long position. We have also taken partial profits on our short-term $TLT trade (+3.8%). Finally, we initiated long positions on $MP and $AJRD. Cash, precious metals and hedges were reduced to 37% in our portfolio which finished 1.64% higher this week.

Here are the top 5 performers of our portfolio this week:

$GILD +16.93% (Drug-Biotech)

$CHTR +11.45% (Telecom Services)

$BWA +9.55% (Auto/Truck-Original Equipment)

$ORSTED.CO +9.54 (Green Energy)

$FIS +9.08% (Financial)

This is our asset allocation as things stand:

– Long stock positions 63% (increased)

– Hedges 9%, though equal to 15% considering leveraged ETFs (unchanged)

– Silver + Gold 3% (unchanged)

– Cash 25% (decreased)

Our currency-adjusted YTD portfolio performance is -3.8% (excl. dividends) vs the European market loss of -15.6% (+11.8% market beat).

Our weekly blog returns after a week of gains for most stock markets with the notable exception of the Nasdaq which finished 1.5% lower and has now lost ground for the third consecutive week: if you are still holding on to the stocks which made great gains in 2020, chances are that you are in the red so far in 2021. There appear to be greater opportunities for capital appreciation in value stocks which also feature good momentum.

The jobs report unexpectedly disappointed and this fuelled a rally on Friday as retail investors pumped more money in the stock market on the assumption that heavy borrowing and low interest rates will continue indefinitely. Despite some of the indices hitting all time highs the risk for a correction is still there which is why it is important not to be fully invested at this time. Scroll below to see what percentage of our portfolio is in cash.

88% of the S&P500 stocks have reported their Q1 earnings so far: the numbers are impressive such that there are several analysts discussing the possibility of this past quarter coinciding with the peak in earnings which would suggest an impending bearish cycle.

Market Performance

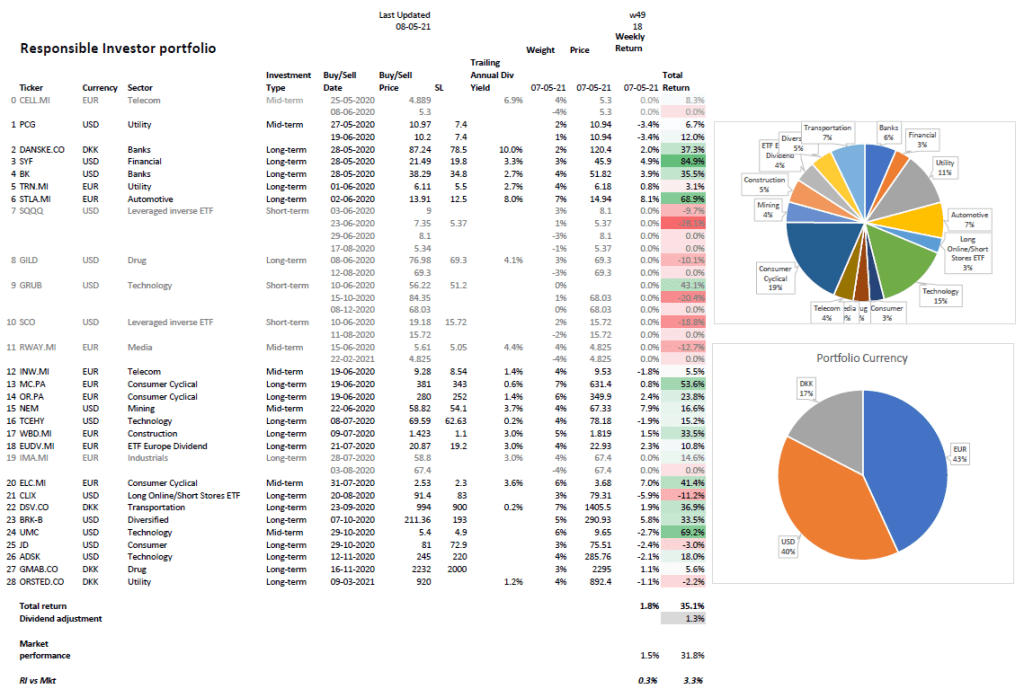

Most of the stock market indices recovered this week following last week’s decline: in the US the Dow was the best performer with a 2.7% gain, followed by the S&P500 which finished 1.2% higher whereas the Nasdaq which finished markedly lower (-1.5%). In Europe, the Stoxx gained 1.8% while the Italian stock market was even stronger and finished 2.0% higher. The Danish OMX20 is on a bullish 9-week streak and was 1.0% higher this week. The US Dollar lost 1.1% on the Euro. Crude $oil gained 2.8% and $Gold showed great strength by appreciating 3.6%. $BTC-USD swung within a 10% range and finished 2.1% higher.

Earnings

Eight of our stocks reported Q1 earnings the week before last:

DSV beat on earnings and revenue

DANSKE beat on net profit

ORSTED missed on revenue

SYF beat on earnings and revenue

UFC beat on earnings and missed on revenue

NEM missed on both the top and the bottom line but the

PCG missed on earnings but beat on revenue and reaffirmed guidance

BRK-B beat on earnings.

$GMAB announced their Q1 earnings on Wednesday with solid gains compared to the same quarter in 2020. The company reported a five-fold increase in operating results and maintained the guidance for 2021 set out earlier in the year. $ELC.MI reported their earnings on the same day and beat consensus as well as raised their guidance: we have a 4.4€ target price on this stock which is already up 41.4% since we bought it.

Next week $JD and $INW.MI will report their Q1 earnings.

Dividends

$OR.PA and $STLA.MI paid their dividend the week before last: our total dividend yield so far is 1.3%. Next week $WBD.MI goes ex-dividend. Our Danish stocks paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 1.8% this week whereas the weighted average of the relevant market indices finished 1.5% higher, which corresponds to a 0.3% market beat.

This week’s portfolio winners were $STLA.MI which was up 8.1% and mining company $NEM which gained 7.9% (+16.6% since initiation) helped by gold strength.

Our Responsible Investor portfolio is now up 35.1% (36.4% including dividends) in 49 weeks and is beating the market by 3.3% over the same period. We are about 64% in stocks & ETFs and 36% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The month-long rally in US stock markets came to a halt at the end of rather volatile week of trading. While the bullish narrative is still considered intact, there are various headwinds which could affect the markets going forward, including the fear of a third wave, rising inflation, and stretched valuations.

Biden’s announcement of the capital gain tax hike took a toll on the stock markets on Thursday, however analysts and investors started reconsidering its impact as early as on Friday on the basis of the fact that it is actually old news and that it only affects less than 1% of the investors.

Market Performance

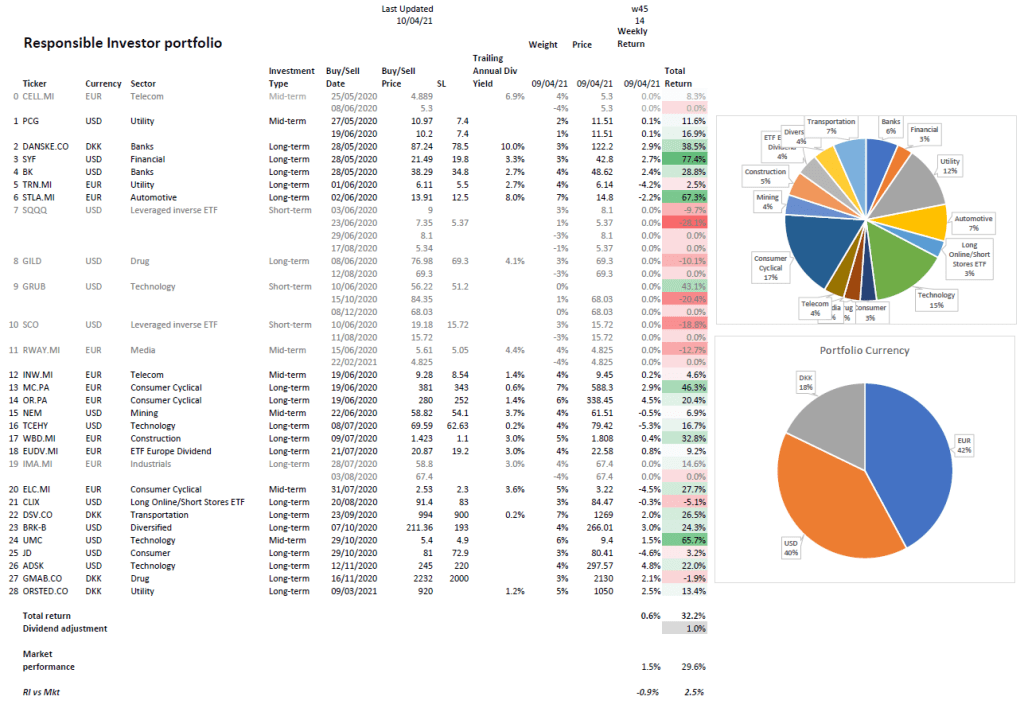

Most of the stock market indices were down up this week: in the US the Dow was the worst performer with a 0.5% decline, while the S&P500 was only marginally lower (-0.1%) followed by the Nasdaq which finished 0.2% down. In Europe, the Stoxx lost 0.8% while the Italian finished 1.4% lower. The Danish OMX20 is on a bullish 7-week streak and gained 1.4% this week. The US Dollar retraced relative to the Euro (-1.0%) for the third week in a row. Crude $oil lost 1.0% and $Gold was flat. $BTC-USD had an ugly week and finished 10.5% lower.

Earnings

While none of our stocks reported earnings this week, dozens of Q1 earnings reports were published: notable ones included $NFLX who beat analysts’ expectations, but missed new subscription expectations and $CMG who rallied on record revenue and triple-digit digital sales growth.

Next week many of our stocks will report their Q1 earnings: $DSV.CO, $DANSKE.CO, $ORSTED.CO, $SYF, $NEM, $PCG and $BRK-B.

Dividends

$MC.PA and $STLA.MI went ex-dividend this week: the former has already paid the dividend whereas the latter will do so next week. Our Danish stocks paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 0.7% this week whereas the weighted average of the relevant market indices finished 0.3% lower, which corresponds to a 1.0% market beat: it is great to finish up on a down week!

This week’s portfolio winners were $UMC which was up 12% and Italian consumer cyclical stock $ELC.MI which gained 4.5% (+31.6% since initiation).

Our Responsible Investor portfolio is now up 33.8% (34.8% including dividends) in 47 weeks and is beating the market by 3.2% over the same period. We are about 63% in stocks & ETFs and 37% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

The US stock markets delivered the fourth consecutive week of gains with all its indices being up more than 1% this week. The bullish sentiment continues to be driven by positive earnings, the impact of stimulus initiatives and positive vaccine/covid-19 data.

The Q1 2021 earnings season kicked off in earnest this week, with several large banks reporting solid numbers: there is however some concern over these earnings already being priced in the current market valuation which could lead to a short term consolidation phase.

On the vaccine front the freeze on the roll-out of the $JNJ vaccine did not seem to affect the estimate of 200 million doses over the first 100 days of vaccinations.

Market Performance

The stock market indices were all up this week: in the US the Dow had a 1.2% gain, while the S&P500 was the strongest index (+1.4%) followed by the Nasdaq which finished 1.1% higher. In Europe, the Stoxx gained 1.2% while the Italian finished 1.3% higher. The Danish OMX20 continued its bullish ride and gained 1.2% this week. The US Dollar retraced relative to the Euro (-0.6%) for the second week in a row. Crude $oil gained 5.7% and $Gold was 2% firmer. $BTC-USD gained 3.4%.

$BK announced better than expected Q1 earnings on Friday but traded 4.4% lower possibly due to many of the other banks stocks showing stronger recovery data. The New York bank’s revenue is still 5% down from last year and the EPS was reported at 0.97$ vs 1.05$ a year ago. Despite this week’s drop, we have gained 23.5% on $BK on the tailwind of a rising interest environment.

In corporate news $MSFT announced the acquisition of $NUAN, its greatest purchase since LinkedIn, which happens just a few weeks after having disclosed being in talks to acquire Discord. $COIN IPO turned out to be a great success.

Dividends

$MC.PA and $STLA.MI go ex-dividend next week. Our Danish stocks paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 0.9% this week whereas the weighted average of the relevant market indices finished 1.3% higher.

This week’s portfolio winners were $MC.PA which was up 7.1% thanks to blow-out earnings and $NEM which gained 6.3% benefitting from the raise in the price of gold.

Our Responsible Investor portfolio is now up 33.1% (34.1% including dividends) in 46 weeks and is beating the market by 2.2% over the same period. We are about 63% in stocks & ETFs and 37% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.

It was another “more of the same” week in the US stock markets with records continuing to be broken and interest rates lacking clear direction. Negotiations on the corporate tax hike are reportedly bringing the two parties to converge on the 25% mark from the initial value of 28%. This increase would see the 2022 earnings shrink by 3%.

Despite the strong employment numbers from the March reports, the fact that the target unemployment rate and the inflation goals are still unmet suggests that the Fed will continue keeping the interest rates unchanged and printing money for the foreseeable future in order to fuel this bull market.

Vaccine roll-out sees increasing volumes in the US, with 3 million daily doses now being the norm and peaks of 4 million achieved for the first time yesterday.

Market Performance

The stock market indices were generally up this week: in the US the Dow had a 2% gain, while the Nasdaq was the strongest index (+3.1%) followed by the S&P500 which finished 2.7% higher. In Europe, the Stoxx gained 1.2% while the Italian index declined 1.2%. The Danish OMX20 had the fifth consecutive week of gains and finished 2% higher. The US Dollar retraced relative to the Euro (-1.2%). Crude $oil declined 2.3% and $Gold gained 0.9%. $BTC-USD was on a rollercoaster this week and finished 0.3% lower.

Earnings

Notable earnings this week included $LEVI which reported a solid beat and positive guidance driven by faster return to pre-pandemic levels expectations and $STZ which traded lower after announcing a revenue and earnings beat as well as a “conservative” guidance: the markets are forward looking and sometimes beating earnings can be offset by weak guidance. Neither of them makes my watchlist due to their high valuations.

The Q1 2021 earnings season will commence next week for our portfolio with $BK scheduled to announce their earnings on Friday together with a number of other major US banks.

Dividends

Our Danish stocks paid their annual dividends earlier this year. Italian stocks traditionally pay an annual dividend in late May. US stocks distribute quarterly dividends.

Portfolio Performance

Our portfolio gained 0.6% this week whereas the weighted average of the relevant market indices finished 1.5% higher.

This week’s portfolio winners were $ADSK and $OR.PA with a 4.8% and a 4.5% gain, respectively. The banks and financial stocks were also strong and outperformed the market. Our two tech Chinese stocks lagged due to pressure exerted by their government.

Our Responsible Investor portfolio is now up 32.2% (33.2% including dividends) in 45 weeks and is beating the market by 2.5% over the same period. We are about 62% in stocks & ETFs and 38% in cash.

The table below summarises the portfolio performance since inception.

If you don’t want to miss my alerts, please subscribe to Responsible Investor or follow me on Twitter. I also run an eToro portfolio which currently has 35+ positions and can be accessed via this link.