Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Is the recent correction just driven by raising interest rates”, and was written on August 19th, 2023.

Weekly summary in a paragraph

The US stock market indices tanked this week, with all major indices finishing lower, most of them for the third week in a row. The European stock market’s downward move was even worse and exacerbated by the Euro depreciating relative to the US Dollar: it has been overtaken by the S&P500 (currency adjusted) for the first time this year. The 2-10y spread reduced significantly this week as long duration yields increased and is still inverted at -66 basis points. The minutes of the last FOMC meeting had a bearish slant. Economic data were mixed with Atlanta Fed GDP standing at 5% versus 4.1% prior and NAHB Housing Market Index coming in at 50 versus 56 consensus. In corporate news, Q2 earnings of Applied Materials beat expectations. There was also a number of strong reports from retail stocks such as Walmart, Home Depot and Target. Despite the vast majority of the S&P500 companies having now reported Q2 earnings, there are still notable ones due to be published next week such as Nvidia, Zoom, Foot Locker and The Gap.

Asset classes weekly performance

This week the Dow finished -2.2% lower (+4.1% year to date) while the S&P500 lost -2.1% (+13.8% year to date), the Nasdaq depreciated -2.6% (+27.0% year to date) and the Russell 2000 was -3.4% weaker (+5.6% year to date). Gold finished -1.3% lower (-0.4% year to date) while Silver gained +0.41% (-8.1% year to date). Crude Oil depreciated -1.4% (+6.8% year to date). The 10-y US treasury yield gained +1.6% (+12.1% year to date). The European stock market fell -3.2% (+13.4% year to date). The Euro lost -0.64% against the US Dollar (+1.5% year to date).

Weekly pitch

When bond yields rise, stocks typically experience a sell-off as investors are lured into putting their savings to work at a relatively low risk. The recent weakness in the stock market may well have been driven by the longer term bond yield rising, but there may be other reasons to justify three consecutive weeks of softness. Last week we warned about the implications of the sharp drop in China’s exports. This week’s focus is on the ailing Chinese housing market which culminated with the news of the country’s largest developer Evergrande filing for bankruptcy on Friday. Chinese bonds have not done well lately and the same applies to Chinese stocks. Until this correction is over, Responsible Investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market.

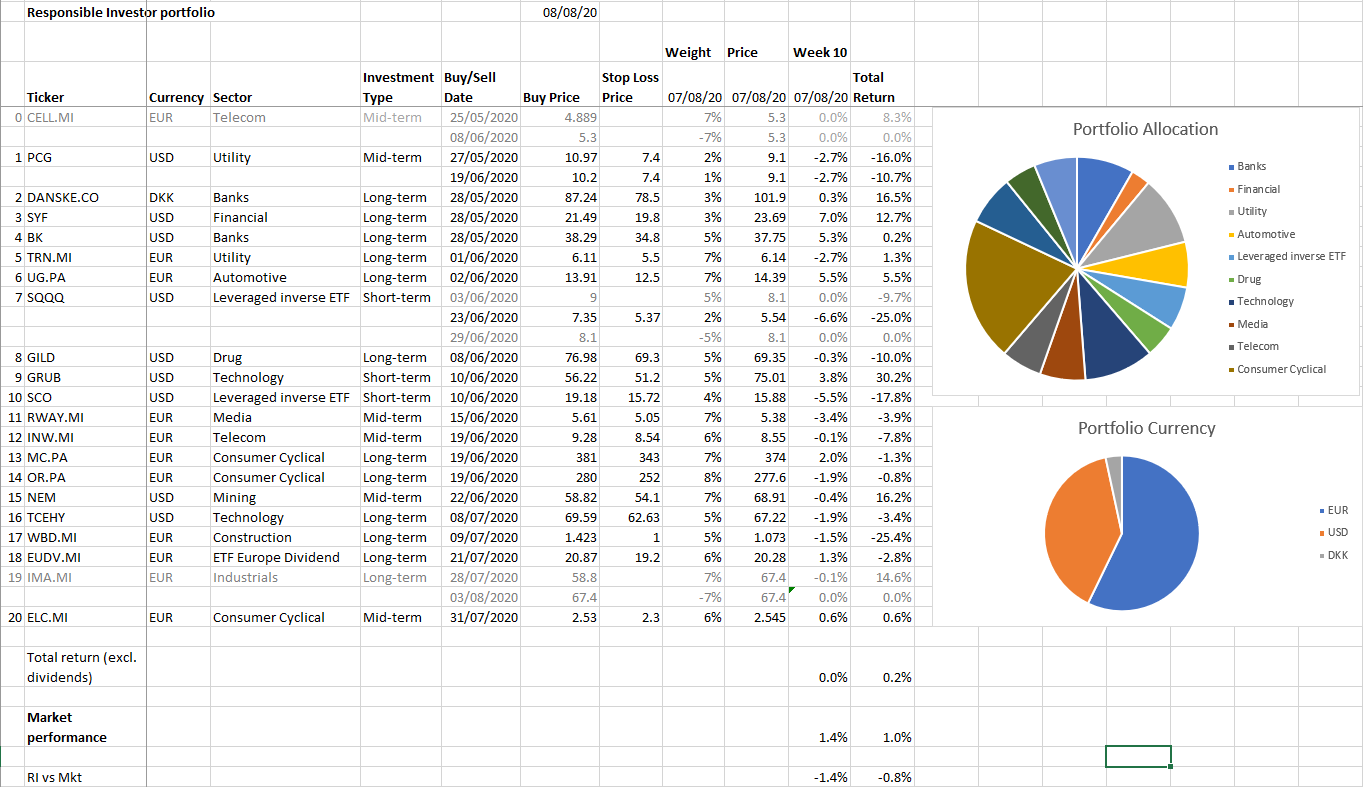

Weekly Portfolio Update

Here are this week’s movements: we have taken full profits on our Molson Coors Brewing short position (+9.7%). We have also initiated a long position on Desktop Metal and accumulated on our Brazil ETF, Newmont Mining and Hershey’s long positions. Sell stops were triggered on our Zimmer Biomet Holdings long position. Cash, US treasury bills, precious metals and hedges amount to 44% in our portfolio (reduced compared to last week). It is mostly thanks to our hedges that we beat the market by +1.0% this week.

Top 5 Weekly Portfolio Performers

ProShares UltraPro Short Russell 2000 +10.7% (3x inverse Russell 2000 ETF)

iPath Series B S&P 500 VIX Short-Term Futures ETN +8.1% (Volatility ETN)

ProShares UltraPro Short QQQ +7.9% (3x inverse Nasdaq ETF)

ProShares UltraPro Short Dow30 +6.8% (3x inverse Dow Jones ETF)

ProShares Short QQQ +2.4% (1x inverse Nasdaq ETF)

Portfolio Asset Allocation

US stocks long positions 47.5% (increased)

EU stocks long positions 8.5% (unchanged)

US stocks short position 2.5% (reduced)

Hedges 8.0% (unchanged)

Silver & Gold 2% (unchanged)

US Treasury bills 2% (unchanged)

Cash 29.5% (unchanged)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is +8.0% (excl. dividends) vs the S&P500 gain of +2.0%, which corresponds to a 6.0% market beat.

Invest responsibly!!!