Responsible Investor is a weekly newsletter and an Apple/Spotify podcast for those who are interested in investing responsibly. Go to responsibleinvestor.dk for more information and to read our disclaimer. This week’s newsletter is titled “Will oversold conditions help the stock market?”, and was written on September 30th, 2023.

Weekly summary in a paragraph

The US stock market indices were mixed this week, as US treasury yields rose and portfolio managers increased spending as part of the end of quarter ‘window dressing’. The European stock market fell for the second week in a row despite better thank expected inflation data in the Eurozone. The 2-10y spread tightened significantly this week and is still inverted at -44 basis points. A strong jobs report and cooler than expected PCE data were this week’s highlights in terms of US economic data. In corporate news, Micron and Accenture guided lower while Nike jumped on strong guidance. Despite the vast majority of the S&P500 companies having now reported Q2 earnings, there are still notable ones due to be published next week such as McCormick, Tilray, Constellation Brands and Levi’s.

Asset classes weekly performance

This week the Dow finished -1.3% lower (+1.1% year to date) while the S&P500 lost -0.7% (+11.7% year to date), the Nasdaq rose +0.1% (+26.3% year to date) and the Russell 2000 gained +0.5% (+1.4% year to date). Gold finished -3.7% lower (-3.2% year to date) while Silver tanked -4.3% (-10.9% year to date). Crude Oil gained +1.2% (+20.4% year to date). The 10-y US treasury yield rose +0.7% (+20.6% year to date). The European stock market gave up -1.3% (+8.6% year to date). The Euro lost -0.68% against the US Dollar (-1.26% year to date).

Weekly pitch

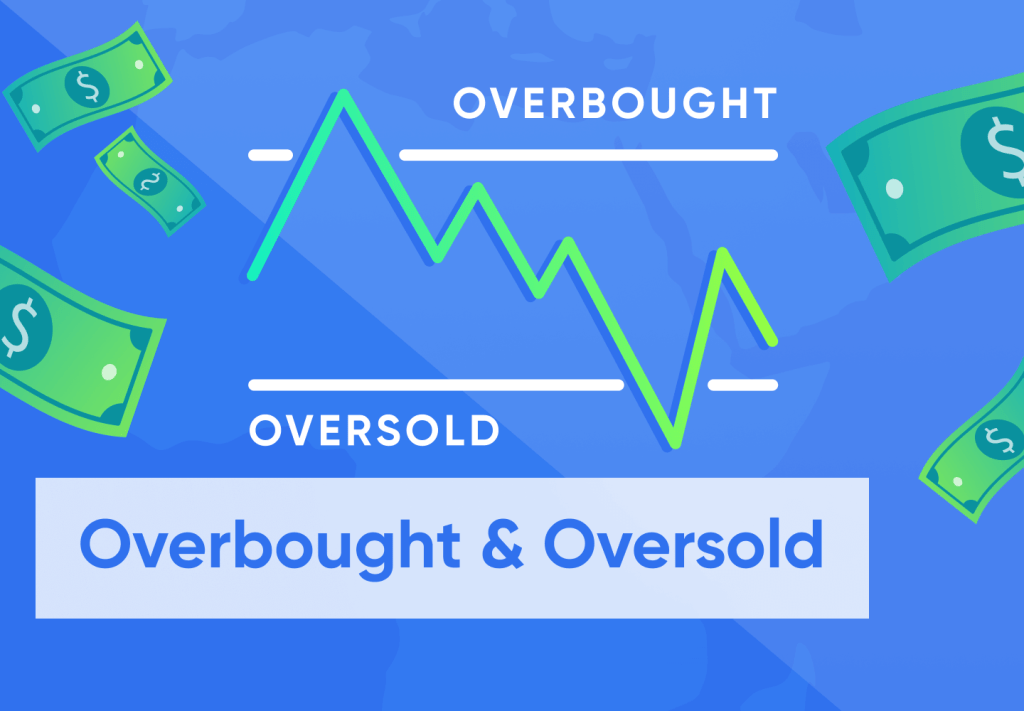

Technical analysis can help assess the market direction from time to time. With the market currently in oversold conditions, there is a fair chance of a bounce. This week’s performance was masked by end of quarter movements. New money pours in at the beginning of the month which might sustain the stock market at the beginning of next week. In the medium term, however, yields are likely to affect where the markets go from here. In the long term, earnings and earnings expectations drive stocks. Responsible Investors should exercise caution and maintain a healthy proportion of their portfolio in cash and hedges as well as a diversified portfolio with some exposure to the European stock market and to emerging markets.

Weekly Portfolio Update

Here are this week’s movements: we have taken full profits on our Ross Stores short position (+8.5%). We have initiated a long position on Boeing and a consumer staples ETF, and accumulated on our Newmont Mining long position. Cash, US treasury bills, precious metals and hedges amount to 38% in our portfolio (decreased compared to last week).

Top 5 Weekly Portfolio Performers

The Gap +6.9% (Apparel)

Callon Petroleum +5.5% (Oil)

ProShares UltraPro Short Dow 30 +4.4% (3x inverse the Dow)

Denbury Resources +2.2% (Oil)

Hilton Worldwide Holdings +1.8% (Hotels & Leisure)

Portfolio Asset Allocation

US stocks long positions 49% (increased)

EU stocks long positions 8.5% (unchanged)

Emerging markets long positions 4.5% (unchanged)

US stocks short positions 0.5% (reduced)

Hedges 7.5% (unchanged)

Silver & Gold 2% (unchanged)

US Treasury bills 2% (unchanged)

Cash 26.5% (decreased)

1-year Portfolio Performance

Our portfolio performance over the last 12 months is +12.6% (excl. dividends) vs the S&P500 gain of +17.8%.

Invest responsibly!!!