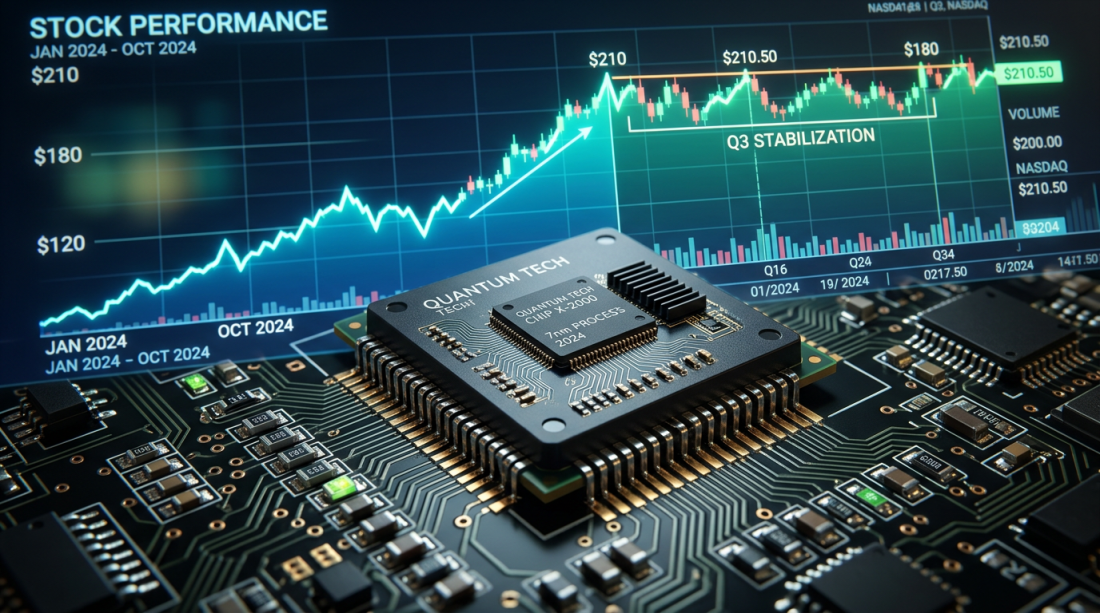

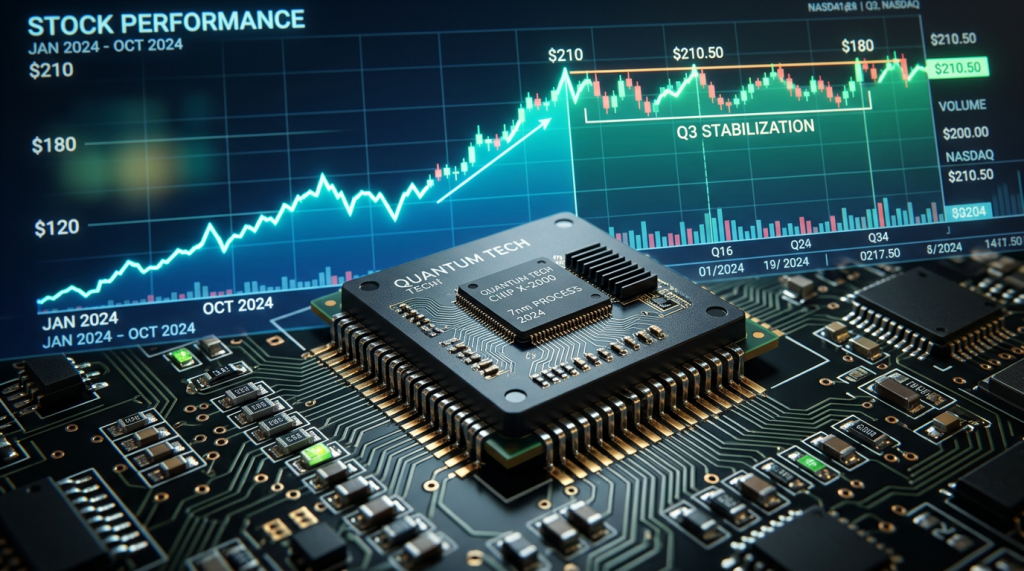

Micron remained a key symbol of the ongoing semiconductor and options frenzy as shares pushed toward new highs after a powerful rally supported by heavy trading volume and aggressive call buying. Market makers continued purchasing stock to hedge positions, helping fuel the surge in $MU. Investors also reacted positively to company guidance suggesting strong memory demand through 2026, although concerns remain that semiconductor demand could slow sharply after 2028.

Momentum across technology stocks stayed strong, with traders continuing to chase artificial intelligence themes tied to $NVDA and other chipmakers. However, broader market strength appeared weaker beneath the surface. Only slightly more than half of companies within the S&P 500 remained in confirmed uptrends, while technology stood as the only sector outperforming the wider index during the past month.

Another speculative wave developed around space related companies ahead of the expected $SPCX public offering, lifting interest in firms connected to exploration and satellite technology, including $NASA. Meanwhile, hopes for easing tensions with Iran pressured oil prices lower, creating additional volatility around energy markets and the oil fund $USO .

Investors remained optimistic overall, but elevated valuations, concentrated leadership, and increasingly overbought conditions suggested the market could face a sharp correction soon without warning.